3/ Do you really want something? Then really work. Half-assing doesn't get you anywhere. Don't look for "system hacks," or whatever, just do it. You first need the baseline mentality of going all in, or nothing else matters

1/ Controversial take: hard work is more important than smart work.

It's a myth that we only have a few hours of good creative work per day. Train yourself to grind long hours first. You will surprise yourself. The work naturally become higher quality, less distracted.

Craziest part is we all knew each other already in high school! Along with @randomjohnnyh (Perplexity cofounder), @demi_guo_ (Pika CEO), @stevenkplus1 and Andrew (Cognition), and many others. We all grew up in different states but met thru the olympiad scene.

Vividly remember this line from @alexandr_wang when we were around 19: "I hear people saying they want to find the next Paypal mafia. Why shouldn't it just be us?"

Glad to see @chameleon_jeff get the recognition he deserves :)

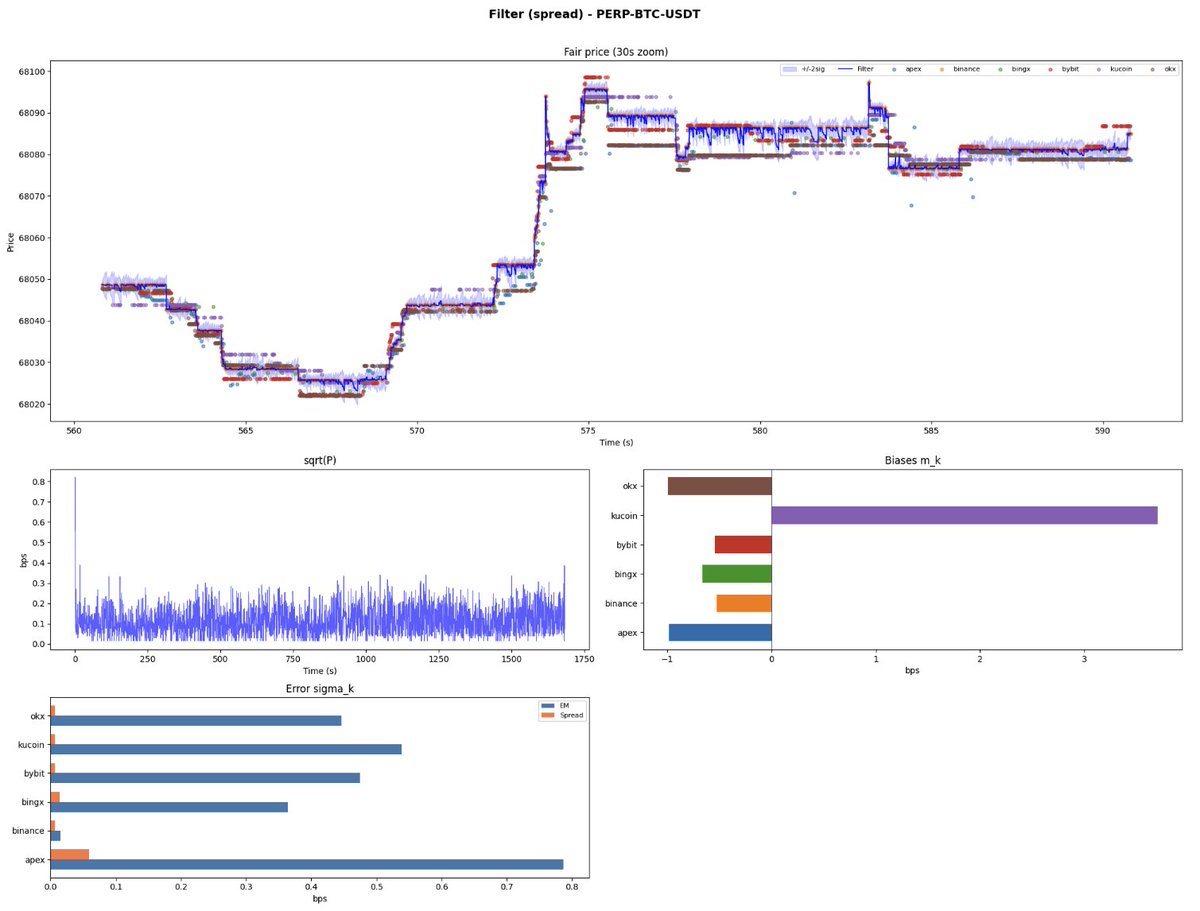

When doing market making or cross exchange arb in crypto we discussed some of the issues of computing fair price from multiple geo-distributed data feeds.

Your quotes will arrive asynchronously from Binance, Bybit, Coinbase and so on, and each will be an indirect measure of fair price.

For example, how do you weigh the Binance and Bybit quotes that came in 35ms and 75ms ago against that Coinbase quote that came in 15ms ago? What about when the ordering is reversed?

Each exchange has a different level of liquidity, error, and basis, so even if the quotes were all equally fresh, there'd still be some decisions to be made. But latency adds an additional layer of complexity.

One mental model for this is ruler theory. Imagine trying to combine the measurements of a bunch of different rulers, each with their own bias (μ) and error (σ), into one optimal measurement.

Bias means a particular ruler is on average off from the truth by a consistent amount. Error means there is a random fluctuation by how much it is off from this average amount, sometimes a lot, sometimes a little, but usually within one stdev around the truth.

In physics, the way to weight each measurement is via precision weighting where each ruler is weighted by its inverse variance:

~ 1/σ²

A quote from a particular exchange is like a ruler measurement of fair price in that it too has its own bias and error.

The dominant part of bias is easy to measure, it is just basis, and a good start is to compute a rolling mean.

Error is a bit more complex. It will depend on liquidity, spread, volatility ... and time elapsed.

BTC-USDT on Binance is expected to be a less errorful measurement of BTC than the same instrument on say, Kucoin. But BTC-USDT on Binance 1 second ago is expected to be more errorful than BTC-USDT on Kucoin 10ms ago.

So there is an innate component to error and a time component. Total error squared will look something like this:

error² ≈ ε²_exchange + σ_price²·τ

where τ is the amount of time that has elapsed from when the quote was emitted to when you registered it, and ε²_exchange is the error unique to that instrument on that exchange (and at that particular point in time). For the time dependence, the assumption here is Gaussian diffusion, which is a defensible first order approximation when you are not near a significant liquidity event.

So errors have a component that grows at a speed proportional to variance, creating a kind of uncertainty cone as they propagate forward in time.

This tells you roughly how to weigh different quotes from different exchanges arriving at different times.

Below are plots from two models built on this intuition. Both are measurably better than just using the Binance mid-quote, and in production, more robust against feed glitches on any single exchange.

We'll discuss in more detail some concrete models that incorporate this intuition, and some that work surprisingly well while ignoring parts of it, in a subsequent post.

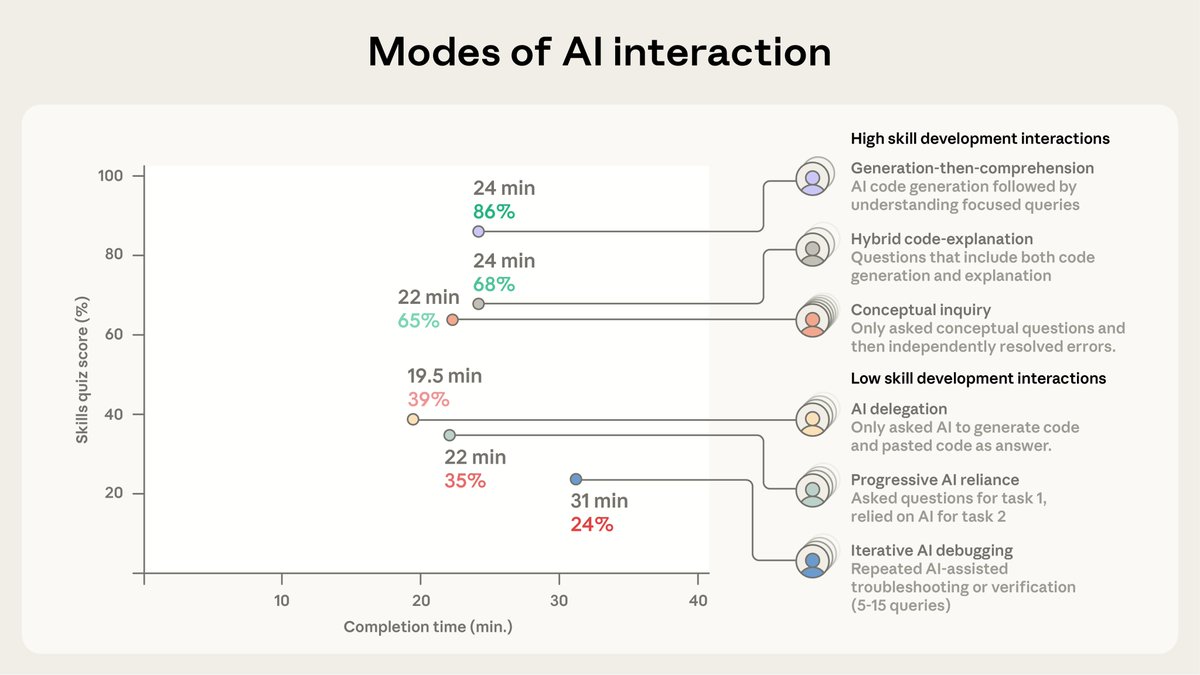

However, some in the AI group still scored highly while using AI assistance.

When we looked at the ways they completed the task, we saw they asked conceptual and clarifying questions to understand the code they were working with—rather than delegating or relying on AI.

This recent talk by Andrew Ng on "Career advice in AI" was interesting. Link below and an automatic summary plus personal comment below [in square brackets].

@macrocephalopod@QuantumInverse@KevinLMak Sum up: Pod shops general don’t recruit retail traders, because candidates who meet those requirements can only come from other pods. If an individual trader could reach that level alone, they wouldn’t need to join a firm.

@profplum99@afekz@OneHotCode1 A priori this can’t be true because you can imagine a systematic strategy which is “do the opposite of what the first systematic strategy does” and they can’t both be structurally short volatility.

Experienced 7-figure+ trader:

Finds an edge, keeps it quiet. Maybe shares with a trusted circle that gives real value back.

Forever NGMI newbie:

Finds an edge, blasts it online, posts stats on Kinfo.

Edge dies in a week/month. Blows up. “Studying harder” again.

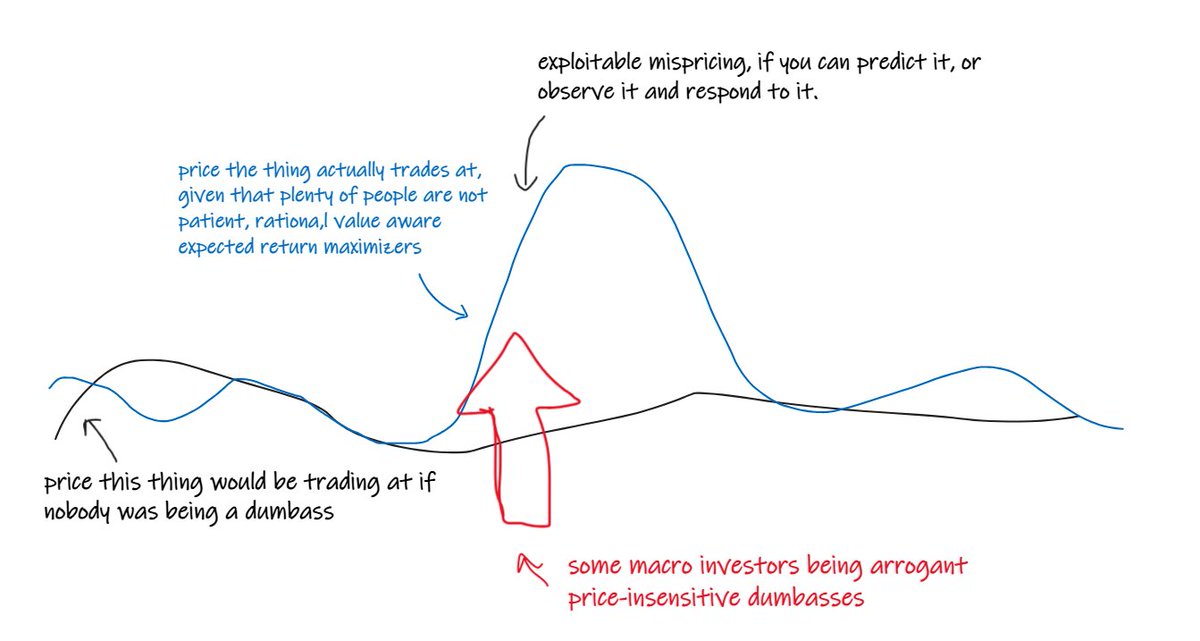

nearly everything that is a good repeatable trading idea looks like:

"under <some circumstances> this thing is likely to be too cheap/rich because <some people> are being forced or greedy or stupid... so the thing is more likely to go up/down in the future"

Thank you to everyone who took the time to thoughtfully respond to my post on transparent markets. I understand that the thesis is controversial and that Hyperliquid is at a new frontier as the first fully transparent order book venue of its scale.

I could well be mistaken, and welcome the continuous dialogue on market structure innovation. However, many criticisms I saw stemmed from misunderstandings, with some points actually supporting transparent systems like Hyperliquid. Market structure is notoriously counterintuitive, and novel approaches often challenge established paradigms, leading to understandable skepticism.

For example, Hyperliquid pioneered protocol-level cancel prioritization, which has since been implemented by new DEXs and even inspired novel transaction ordering ideas on other blockchains. But at the time, it was considered controversial because it went against traditional market design. I hope that transparent trading will follow a similar path to adoption.

I may have been too ambitious trying to cover a complex argument in a single post. Given the specific patterns in criticisms, I'd like to take this opportunity to zoom in on nuances that were missed in the high level summary. What follows is an argument for the final state of efficient markets, with the understanding that Hyperliquid is far from fully efficient today. However, inefficiency is opportunity for those hungry to act. Hopefully this post can also be a call to action for traders, market makers, and builders to translate transparent markets into the highest quality execution venue for all.

--

Before delving into specific concerns, let’s crystallize some counterintuitive principles that can form a helpful mental model for market structure:

1. Counterparty principle: Benefits of counterparty curation are misattributed to privacy.

Users ultimately care about execution. As studies have shown though, privacy sells. Alternative trading venues often market privacy as the causal feature for improving execution. In reality, the primary source of benefit for users is the screening of counterparties allowed to participate on the venue. Hyperliquid’s market design provides these same benefits more directly and effectively than patchwork solutions. Hyperliquid’s solution also democratizes access, improving execution for all traders large and small.

Note that transparency does not mean doxxing. Of course, the exact identity of some traders will fundamentally change the value of the asset. But those traders need not dox themselves, e.g. Warren Buffet can buy BTC and benefit from transparent markets, without tying his identity to his address.

2. Competition principle: Maximizing competition is key to improving execution.

Many traders who want to execute in size have some form of alpha. However, the group of informed medium/long term traders in aggregate is difficult to distinguish even over yearly timeframes, as their realized sharpe is too low for statistical significance. It is challenging to distinguish between a trader with solid medium term alpha and a degenerate gambler who got lucky. Therefore, while the desire to minimize market impact and alpha leakage is natural, it’s usually outweighed by the improved liquidity from transparent markets.

Traders therefore see improved execution despite revealing their strategy, as market makers are bound to provide liquidity to the entire range of flows in the market. Competition is the bedrock of capital markets and economics. As an example, the Hyperliquid order books support an onchain TWAP. Such a broadcasted intent to trade is in fact a reasonable proxy for optimal execution. Market makers will immediately fill some size so that the earlier TWAP orders receive worse execution, but will also compete to fill the remaining flow. The competition between market makers ensures near optimal overall execution over the course of the TWAP. Any inefficiency in execution is an opportunity for another market maker to undercut the others.

3. Repeated games principle: Execution improves when one-time games become repeated games.

Market makers evaluate each decision from a game-theoretical framework, as they are in the business of making positive expectancy bets. On Hyperliquid, every account placing more than one order is playing a repeated game. Repeated games have dramatically different optimal strategies from the one-time games of private venues, and the resulting equilibrium is better execution for everyone other than toxic extractors. Competition is essential for the optimal market marker strategy to benefit the end user, which is amplified by the next principle.

4. Full transparency principle: Benefits from transparency are non-linear and only manifest when transparency is at the system level.

When optimizing for execution, “the system knows” > “no one knows” > “some people know.” The worst of the three states is where some insiders have privileged information. Those insiders can act exploitatively to extract profit from end users. Because L3 books are not transparent in tradfi, the “darker” venues often implement systems to unilaterally apply counterparty-specific filtering to trades. Hyperliquid achieves the same effect on a lit venue and therefore maintains the benefits of efficient order book execution.

--

Common criticisms to the initial post, and my responses [I’ve bracketed references to the different principles]:

1. Many large desks in tradfi trade OTC, which is evidence that public venues cannot support large size.

Response: This point actually supports Hyperliquid. In tradfi's L3 books, there is no reliable way to broadcast your identity trustlessly to all counterparties. Using an OTC desk is a compromise, telling a small set of professional counterparties that you are non-toxic. Like trading on an L4 order book, trading OTC is a repeated game where the OTC desk is quick to ban any counterparties that adversely select a small fraction of quotes, or engage in otherwise toxic behavior [repeated games principle]. The OTC desks offer quotes where their own algorithmic execution/hedging costs are below the markup, which is only possible when their fills’ immediate markouts are positive.

A Hyperliquid whale who places an onchain TWAP order is effectively routing their flow to every "OTC desk" plugged into Hyperliquid. When OTC counterparties expand from a select few to all market makers, the competition improves execution for the user compared to the bespoke OTC quote [competition principle]. In summary, execution on Hyperliquid incorporates the efficiency of lit venues with the counterparty signaling of OTC. This high quality execution is available to all users equally.

2. A large percentage of tradfi volume happens on dark pools, retail internalizer systems, etc.

Response: This argument also supports Hyperliquid. The basic idea behind dark pools is that two large whales with a "coincidence of wants" can match immediately and bypass the spread that lit markets charge. Until such a match exists, orders are attempted to be kept private to reduce market impact. While a neat idea at first glance, the privacy of dark pools is unlikely to meaningfully protect intentions or improve execution. For example, sophisticated actors participate in dark pools themselves. At a minimum, their fills are a strong signal on the supposedly private flow. This shares many parallels with the insider information discussed in the following section. Information that will be deduced anyway is better made public [full transparency principle].

As another argument against the effectiveness of privacy properties, dark pools rely heavily on participants having identities known to the pool operator [repeated games principle]. This is necessary because the private information is easily leaked. There are strict requirements for participation, e.g. high fill rate, minimum order size, and negative short term markouts. Offenders with toxic behavior are banned or deprioritized [counterparty principle]. Like OTC desks discussed above, transparent L4 books on Hyperliquid incorporate and improve upon many of these positive properties of dark pools within an open, systematic framework.

3. Public data allows hunting of liquidations/stops.

Response: Most would agree that unlike size information, preserving margin privacy is beneficial for the end user. Perhaps a ZK privacy implementation can accomplish this in the future. However, until then, users are less likely to be successfully hunted if everyone knows liquidation and stop prices than when only the exchange operator knows [full transparency principle]. Two reasons:

a. On CEXs, your position information is far from private. Based on empirical data of insider trading leading up to listings, one should assume that liquidations and stops are also vulnerable to misuse. This can be despite best efforts from management: it is extremely difficult to completely control large organizations from leaking information. When insiders hunt stops and liquidations, there is no public data for other market makers to understand the source of the temporary dislocation. This decreases the required capital to successfully push the price.

b. In the game theoretical equilibrium of transparent data, stop and liquidation hunting are likely unprofitable endeavors on average. Whales are protected by the entire system of market participants acting rationally. People trying to hunt liquidations and stops will be counteracted by people trying to trick them into the hunting. For example, someone who wants to open a large long position can execute half of their position on high leverage, bait the hunters to short, then increase collateral and enter the remaining desired position at a more favorable price. As long as some profit seeking “anti-hunters” exist, all whales benefit from the cover.

While point (b) will take time to play out, markets are ultimately efficient. Even before this equilibrium is reached, the full transparency principle in point (a) suggests Hyperliquid's model offers more robust protection for whales. Liquidity is generally deeper when lit venues are more transparent [competition principle], which further increases the cost of liquidation and stop hunting.

4. Some users have alpha and will not benefit from transparency.

Response: The users that are disadvantaged by Hyperliquid’s system are a very small set of “toxic” participants. These are the same adversarial traders that dark pools, OTC desks, and other solutions try to avoid. A small number of professional HFT firms have alpha on this timescale, and it’s a failing of traditional market structure that these toxic takers have the ability to tax all other users of the system.

As an aside, short term alpha and toxicity is a continuous spectrum, so I’m oversimplifying for sake of argument. For example, there are intraday quantitative strategies that can realize significant sharpe ratios, whose flow could be a reliable momentum signal for market makers. The technical reason this is not a problem is that cost to rotate accounts is proportional to fee sensitivity of the strategy, which is inversely proportional to the time it takes for others to detect the strategy with statistical significance. In other words, the more execution matters to a quant strategy, the less the burden of obfuscation.

Regardless, the vast majority of users on Hyperliquid do not fall remotely close to this category of quantitative, toxic alpha. Note that “toxic” does not mean “informed,” but rather traders who profit non-constructively from slight infrastructural or other structural advantages such as latency. Hyperliquid's cancel prioritization and L4 order book essentially boost the short term liquidity available to non-toxic small and large orders, respectively. As a conservative lower bound, as long as market maker counterparties on Hyperliquid can hedge in time on other venues, the trader benefits from Hyperliquid’s system.

--

I know I’ve missed other points, but will stop here to keep this post digestible. Thanks again to everyone for their thoughtful feedback, especially those who took time to review an earlier version of this post. I look forward to continuing this discussion!

Psychologists have posited hundreds of cognitive biases over the years. A fascinating new paper argues that they all boil down to one of a handful of fundamental beliefs coupled with confirmation bias.

[Link below.]

![SteveStuWill's tweet photo. Psychologists have posited hundreds of cognitive biases over the years. A fascinating new paper argues that they all boil down to one of a handful of fundamental beliefs coupled with confirmation bias.

[Link below.] https://t.co/pQ2elnxRo1](https://pbs.twimg.com/media/GoNMoV2bEAAL_Yb.png)