@Octop3s What you've just said is the truth.

They thinks being gated with gradual access codes would create a kind of demand. In an industry where you have new competitors daily?

Most lending markets optimize for liquidity and capital efficiency first, then try to manage risk after the fact while @sparkdotfi ’s security/risk framework is one of the better examples of where DeFi lending is heading.

The whole architecture is built around bounded risk, controlled capital movement, layered loss absorption, oracle redundancy, and stress-response mechanisms.

Here’s how Spark does it.

—

Spark keeps a deliberately narrow collateral set, which reduces exposure to fragmented liquidity, weak redemption assumptions, and long-tail collateral risk.

Instead of trying to list every possible asset, it prioritizes predictable liquidation behavior and deeper market structure during stress.

For assets with more unique or chain-specific risks, Spark uses isolated markets. That means risk can be priced more precisely per collateral type, and a single collateral issue does not automatically contaminate the broader pool.

—

The oracle setup is also important.

Spark uses a three-oracle median system drawing from @redstone_defi , @chainlink , and @ChronicleLabs oracle.

When all three return valid prices, the median is used. If only two valid sources are available, the average is used, with fallback logic under degraded conditions.

That reduces dependency on any single oracle provider.

For pegged or exchange-rate assets like $wstETH, $weETH, $cbBTC, $WBTC, and $LBTC, Spark adds another layer through a killswitch oracle.

• This continuously checks whether market pricing is diverging from the underlying exchange-rate or redemption value.

• If deviation passes predefined thresholds, Spark can halt new borrowing against that collateral.

That is a very important safeguard because it prevents users from borrowing healthy debt against impaired collateral during periods of stress, liquidity fragmentation, or pricing dislocation.

—

The liquidity architecture is another strong part of the design.

Spark’s Liquidity Layer is not just idle capital sitting passively in a pool. It coordinates liquidity across Spark Savings, SparkLend, the Sky PSM, and other approved venues.

But the key part is that this liquidity movement is constrained by design.

All venues must be pre-approved by governance. Capital movement is subject to;

• allocation limits

• rate limits

• min/max inventory bands

• risk parameters

• operational boundaries

Spark’s framework is built around controlled risk, not unlimited automation.

Capital can only move through approved venues, rate limits, allocation limits, and governance-defined boundaries. So even if automation fails, the damage is contained.

The same idea applies to losses.

Before depositors are affected, losses pass through multiple buffers: risk capital, surplus buffer, Genesis Backstop, SKY backstop, and final resolution.

Spark Savings also has 1:1 USDS backing, liquidity buffers, fast withdrawal routing, real-time transparency, Credora risk reviews, and limited bridge exposure.

—

Overall, the theme is simple:

Spark is not just chasing higher yields.

It is building DeFi credit infrastructure around constrained liquidity, layered protection, and limited blast radius.

Inside Spark’s loss absorption & risk frameworks.

Spark’s security architecture is designed around:

• bounded capital movement

• explicit loss absorption layers

• coordinated liquidity management

• multi-layered oracle systems

• constrained automation under governance-defined limits

This deep dive breaks down how Spark structures risk, liquidity, and loss absorption across Spark Savings, SparkLend, and the Spark Liquidity Layer before losses propagate toward user deposits.

Including:

• updated loss absorption waterfall

• Prime Agent risk capital

• Genesis Capital Backstop

• oracle and killswitch architecture

• programmatic liquidity coordination

• constrained allocation design under stress

Security by design.

Resilience by architecture.

See what sits between losses and user deposits: https://t.co/JQrfSxMB4z

@andrewmoh@aave Forks only matter when they improve the original design.

Aave V3 works because it took an already trusted lending model and pushed it further with better efficiency, integrations and risk controls.

RWA value has surpassed $31.5B onchain, with tokenized stocks growing 374% and credit expanding 289% year-over-year.

Yet the most important shift is not asset tokenization itself, but the race to solve liquidity, distribution, and DeFi integration.

Here's what's actually happening:

—

● The RWA Experiment Is Over

RWAs have surpassed $31.5B in distributed value, while the broader represented asset market now exceeds $407B across public blockchains.

• Tokenized Stocks: +374% YoY

• Tokenized Credit: +289% YoY

• Commodities: +215% YoY

• Real Estate: +130% YoY

Growth is no longer coming from a single category, with capital now flowing across equities, credit, commodities, and real estate.

The industry has already proven demand for onchain assets, making infrastructure and market depth the next major battlegrounds.

—

● Why Treasuries Became Crypto's First Institutional Asset Class

Tokenized U.S. Treasuries have grown into a $14B+ market, making them the dominant gateway for institutional capital entering onchain finance.

• @BlackRock $BUIDL

• @OndoFinance $USDY & $OUSG

• @circle $USYC

Treasuries offered the ideal bridge between traditional finance and DeFi by combining familiar risk profiles, regulatory clarity, and yield-bearing exposure in an onchain format.

This is why government bonds continue to dominate RWA markets today, establishing the foundation before more complex asset classes can scale.

—

● The Next RWA Battle Is Not Asset Issuance

Tokenizing assets is no longer the hard part, as infrastructure for bringing stocks, bonds, and other real-world assets onchain already exists.

Projects like @xStocksFi and @XLayerOfficial are drawing attention because they are tackling a much bigger problem: distribution, liquidity, and user access.

Without active markets and efficient distribution channels, tokenized assets remain digitally wrapped products rather than financial assets.

Long-term winners will be determined by liquidity, distribution, and user access, not by asset issuance alone.

—

● The Largest RWA Opportunity Is Still Untapped

Despite the rapid growth of the sector, only around $3B is currently being utilized as DeFi collateral.

• ~$3B used in DeFi

• ~10% utilization

• ~90% remains outside DeFi

The largest opportunity now lies in making existing RWAs productive inside DeFi.

The assets already exist. The missing piece is composability.

—

● RWA Infrastructure Is Serving Two Different Markets

As the sector matures, RWA adoption is increasingly splitting between DeFi-native users and institutional allocators.

DeFi Users:

• Leverage

• Yield loops

• Collateral efficiency

Protocols like @pendle_fi, @Morpho, @eulerfinance, and @Aave are designed around these needs.

Institutions:

• Compliance

• Audits

• Reporting

Products such as @BlackRock's $BUIDL, @FTI_US's $BENJI, and @WisdomTreeFunds are built around these requirements.

Future RWA platforms will need to serve both groups without sacrificing composability or compliance.

—

● The Broken Token Problem

Many RWA businesses are growing, but their tokens are not.

Revenue -> Company

Yield -> Asset/SPV

Token -> Governance

Value accrues to the company and underlying assets, while token holders often capture little of it.

This creates a growing disconnect between business growth and token value.

—

The next phase of RWAs is not about tokenizing more assets, but about financializing them through lending markets, perps, vaults, RWA-backed collateral, and sustainable value accrual models.

The first phase proved that real-world assets could move onchain, while the next phase must prove they can become liquid, composable, and economically useful within DeFi.

The projects that solve liquidity, composability, and token value capture will define the next decade of tokenized finance.

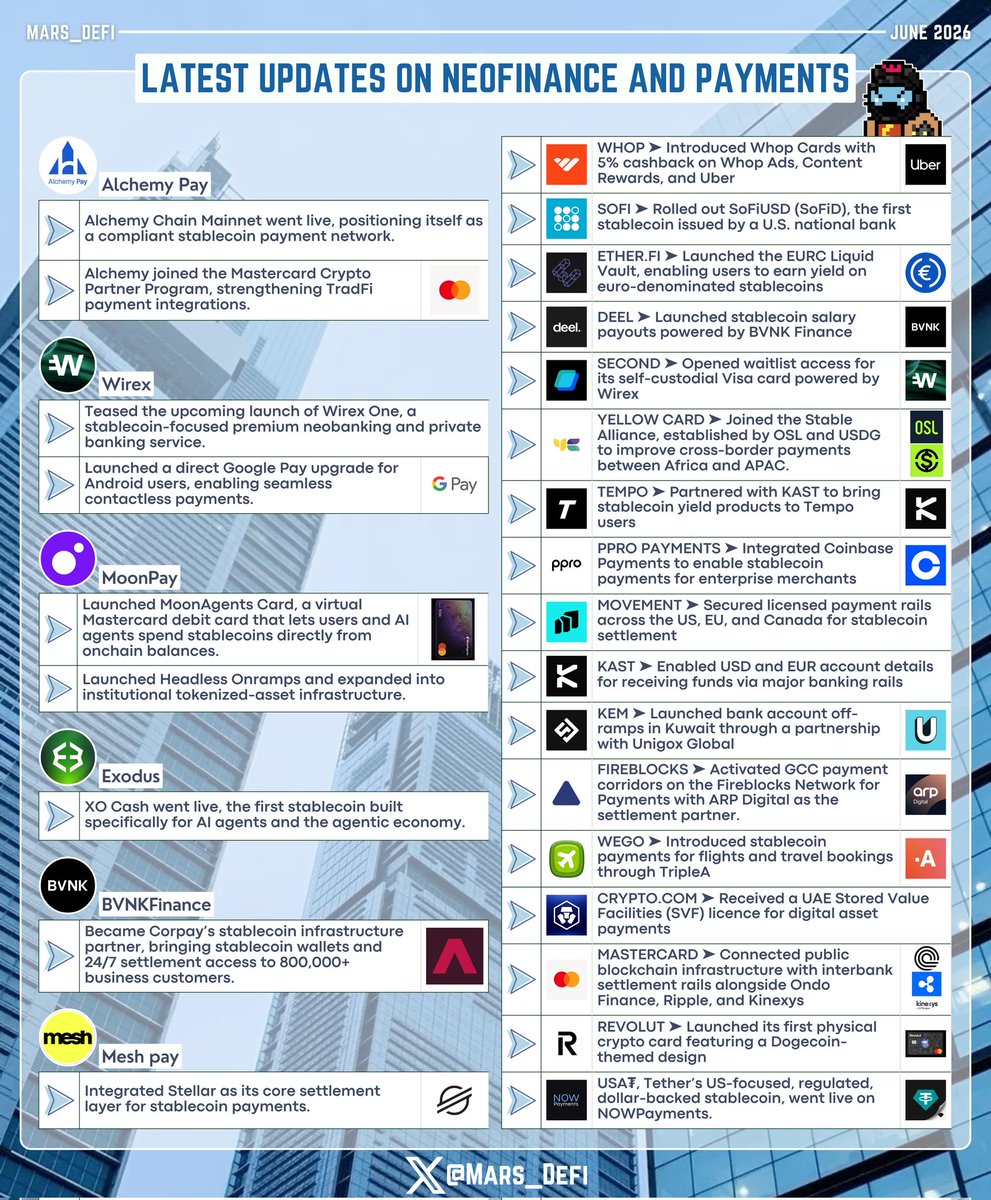

May marked another step forward in crypto’s transition from speculation to financial infrastructure.

While headlines remained focused on markets and token performance, the NeoFinance stack continued shipping products that bring stablecoins and digital assets closer to everyday financial activity.

Across payments, banking, payroll, remittances, and settlement infrastructure, teams spent the month expanding access, improving user experience, and strengthening connections with TradFi systems.

Here’s a comprehensive breakdown of what shipped across the NeoFinance and payments landscape in May.

—

● @AlchemyPay

• Alchemy Chain Mainnet went live, positioning itself as a compliant stablecoin payment network

• Alchemy joined the @Mastercard Crypto Partner Program, strengthening TradFi payment integrations

● @wirexapp

• Teased the upcoming launch of Wirex One, a stablecoin-focused premium neobanking and private banking service

• Launched a direct Google Pay upgrade for Android users, allowing cardholders to add their Wirex cards to Google Pay for seamless contactless payments

● @moonpay

• Launched MoonAgents Card, a virtual Mastercard debit card that lets users and AI agents spend stablecoins directly from their onchain balances

• Launched Headless Onramps and expanding into institutional tokenized-asset infrastructure

● @exodus

• XO Cash went live, the first stablecoin built specifically for AI agents and the agentic economy

● @BVNKFinance

• Became @CorpayFX’s stablecoin infrastructure partner, bringing stablecoin wallets and 24/7 settlement access to 800,000+ business customers

● @meshpay

• Integrated @StellarOrg as its core settlement layer for stablecoin payments

● @whop

• Introduced Whop Cards, offering 5% cashback on Whop Ads, Content Rewards, and Uber

● @SoFi

• Rolled out SoFiUSD (SoFiD), the first stablecoin issued by a U.S. national bank and redeemable 1:1 for cash or cash equivalents

● @ether_fi

• Launched the $EURC Liquid vault, allowing EtherFi users earn on their Euros

● @deel

• Launched stablecoin salary payouts, powered by @BVNKFinance

● @secondfiapp

• Opened access to waitlist for their self-custodial Visa card, powered by @wirexapp

● @yellowcard_app

• Joined the Stable Alliance, established by @osldotcom and @usdgo_official to improve cross-border payments between Africa and APAC

● @tempo

• Partnered with @KASTxyz to bring Kast’s stablecoin earn product to Tempo

● @PPRO_Payments

• Integrated with @Coinbase Payments to bring stablecoin payments to enterprise merchants

● @movement_xyz

• Secured access to licensed payment rails in the US, EU, and Canada to become the stablecoin settlement and yield layer for emerging markets

● @KASTxyz

• USD and EUR account details went live, allowing users to receive USD via ACH, Fedwire, or SWIFT, and EUR via SEPA

● @kem_app

• Launched off-ramps to bank accounts in Kuwait, in partnership with @Unigox_global

● @FireblocksHQ

• GCC payment corridors went live on the Fireblocks Network for Payments, with @ARPdigital_io as the regulated corridor settlement partner

● @Wego

• Introduced stablecoin payments through partnership with @TripleAHQ for flights and travel bookings

● @cryptocom

• Received a UAE Stored Value Facilities (SVF) licence for digital asset payments

● @Mastercard

• Partnered with @OndoFinance, @Ripple, and Kinexys by @JPMorgan for a landmark transaction connecting a public blockchain with interbank settlement rails

● @Revolut

• Launched its first physical crypto card, a Dogecoin-themed card with zero exchange fees

● @NOWPayments_io

• USA₮, @tether's US-focused, regulated, dollar-backed stablecoin, went live on NOWPayments

—

The NeoFinance stack is still evolving rapidly, but it’s becoming difficult to ignore that crypto payments are no longer a future use case. They are steadily becoming part of the global financial system.

I’ll be honest, $BTC doesn’t look great here.

From a higher-timeframe perspective, structure is still bearish, and until price reclaims key levels with strength, it’s hard to argue for a clean bullish reversal.

Right now, $BTC is trading into its final major demand zones. These are the areas bulls need to defend if they want to keep the broader range alive.

The key level for me is $60k.

That zone has acted like the most protected demand area on the chart. If BTC loses it cleanly, I think sentiment gets much worse and the market starts pricing in deeper downside.

For now, I’m not trying to force bullishness.

Either BTC defends demand and shows a proper reclaim, or we respect the downtrend.

Another product looks like it is quietly hitting PMF as @Collector_Crypt’s growth is hard to ignore here.

From the data, monthly volume moved from almost nothing around late 2024 to nearly $200m in May 2026.

Gross revenue followed the same path.

January 2025 was barely above $1.1M in gross revenue and by May 2026, that number had grown to over $102m.

The more interesting part is the consistency of the growth curve:

Volume keeps expanding, revenue keeps following, and activity is not disappearing after the first wave of users.

—

That is usually where real PMF starts to show.

A lot of crypto products can attract attention once but very few can retain users after the initial novelty fades.

Collector Crypt seems to be doing the harder part which is turning utility into repeat usage.

The product gives users a reason to keep coming back, whether through collectibles, packs, trading, or the broader gamified experience around tokenized assets.

And that matters because retention is what separates hype from infrastructure.

h/t : @Blockworks