Monthly VC/LP debrief.

What I actually saw in May 2026:

1/ SF is in full gold rush mode again, but history says the current winners won't stay on top forever. Every dominant technology eventually gets surpassed – newspapers, telecom, cable, Google in ads, IBM in computers. In AI the same pattern is already playing out: compute will hit walls, chips get dramatically more efficient, new energy sources emerge, and entirely new model architectures appear. The people feeling left behind today may just be early in a much longer cycle. (h/t @TurnerNovak)

2/ The largest $10B+ funds went from 140–150 collective early-stage deals per year in the SaaS era to 370–400 in the AI era. But the concentration is at the top of the market – top-decile rounds, known founders, proven operators. @kevinhartz calls it "option value": a small check today for the right to lead Series A tomorrow. The average seed round remains territory for EMs.

3/ We might be entering a Zombie VC era. ~85% of 2017–2018 vintage funds still haven't returned 1x DPI after 7–8 years. Median DPI sits at $0.34 on the dollar, while median IRR for the same cohort looks respectable at 11.6%. Paper returns hide the reality. The liquidity window opening over the next two years will be the moment of truth for most of these funds.

4/ @SpaceX IPO might be the single largest DPI event in VC history dropping into the lowest-distribution moment in venture capital history. @foundersfund alone, with an early $20M check in 2008, could return $60B+ (~3000x). When that capital hits LP accounts, it needs to be redeployed and that will circulate a new wave of fundraising for the same funds and fresh allocations from LPs who finally have liquidity to work with.

5/ The @cerebras IPO was the first real data point on crossover returns after two years of everyone writing off the model – both early-stage VCs and late-stage crossover funds made money on the same company, and LP conversations shifted from "do we have any exposure to the winners" to "how do we get into the next one." The same strategy that was declared dead in 2022-2023 got fully rehabilitated by a single exit. (h/t @MeghanKReynolds)

6/ Monte Carlo across 1,391 VC funds: concentrated portfolios (15 companies) and diversified ones (100 companies) produce the same average fund return – 2.44x. But compounded across multiple vintages, diversified wins: 2.25x vs. 1.78x. Concentrated funds carry more variance per fund, and variance drag compounds against you over time. The extreme outcomes (15x+) are almost exclusive to concentrated funds but the probability is tiny either way. (h/t Steve Kim)

7/ EM activity is showing the first real pulse in years. @cartainc logged 78 new US venture funds in the $10M–$100M range in Q1 2026 – a 34% jump from Q1 2025. Still well below the 2022 peak of 147, but the post-winter bottom might finally be in. The managers raising right now are doing it without a favorable macro, without easy LP recycling, and into a market where mega-funds are more active at seed than ever. (h/t @PeterJ_Walker)

8/ 76% of all EM-focused FoFs are American. The entire addressable market for a Fund I or Fund II isn't 132 FoFs – it's roughly 33. The other 100 exist, but Classic and Government-Led FoFs structurally can't anchor an early-stage vehicle: the check size doesn't justify the overhead, and a pension board can't be sold on a first-time manager without a track record. Geography and fund type filter out 75% of the market before the first meeting. (via @murphcapital)

9/ The 10-year fund is structurally mismatched with the assets mega-funds are holding. @SpaceX has been private for 18 years. @stripe for 15. For managers at that scale, @sequoia's move makes sense – open-ended, permanent capital, indefinite horizon. For small funds the logic runs the opposite way: the 10-year horizon enforced as a hard constraint, secondaries at Series C/D as the default exit, actual distributions on schedule. (h/t @credistick)

10/ There are only 3 positions that matter in a startup's cap table story: first investor, most helpful investor, biggest investor. Biggest is reserved for ~10 megafunds. First requires conviction most managers don't have – and LP preferences for concentrated portfolios often push against it structurally. So 90%+ of firms end up competing for "most helpful," which is why every pitch deck has a platform slide and every GP talks about their right to win oversubscribed rounds. (h/t @arian_ghashghai)

Every month I track new fund launches, LP events, market reports, and what's actually moving in VC/LP.

All of it in the @murphcapital newsletter: https://t.co/Wi8pAGQHLB

Or ... instead of blaming the employees, maybe companies realize how lousy they've become at training, and investing in humans to make them more effective may become management mantra again.

The equation is fairly straightforward:

Competent employees x AI tokens = Accelerating business & market share gain

Incompetent employees x AI tokens = slop

Companies are now realizing they have a lot of shitty employees.

They aren’t going to permanently cut spend on tokens. They can’t afford to because of game theory.

So instead they will fire the employees they believe are incompetent to make room for higher token budgets for those that are competent.

Lots of orgs however have a managerial class that doesn’t optimize for share gain and winning in general.

Thats fine. A wave of startups and existing platforms who can effectively leverage AI to expand scope of their business will crush the incompetent at a rate that will leave analysts and managers dizzy.

Change is coming. Fast. And reflexively the faster the change the higher the panic the lower the ROI threshold the more revenue and capital accrues to the labs the faster the models improve. And so on.

Mostly true. What matters is securing the long-term future of consciousness, both on Earth and other heavenly bodies.

We cannot just focus on Earth, because there are irreducible external (eg massive meteor) and internal (eg global nuclear war) cataclysmic risks.

The Moon is faster to make self-growing, but is more susceptible to problems on Earth. Mars will take longer to make self-growing, because it is so hard to reach, but is more secure from Earth disasters for that same reason.

Both the Moon and Mars should have self-growing civilizations. Making this happen is the prime directive of SpaceX.

I just got back from SF and I FEEL INSPIRED.

I spent 5 days with frontier AI model teams, AI startup founders, and 3 billionaires.

My takeaways:

1. I had lunch with 3 billionaires. All of them are buying SaaS companies and rebuilding them agent-first. They were deeply inspired by Bending Spoons and Ryan Cohen's eBay deal. Buy the company, cut the headcount, rebuild the tech, add agents, add features, make more valuable experience, raise prices.

2. The frontier model companies are hungry for usage data from the field. They can see API calls and token counts. They can't see the actual workflows. If you're deep in a niche using these models in ways the model companies haven't seen, that understanding is incredibly valuable. Usage intelligence is the new alpha.

3. Consumer AI is massively underbuilt. Every billboard in SF is either B2B inference infrastructure or vertical agent companies. The entire city is optimized for enterprise. Meanwhile you have companies like Cal AI doing $50M ARR in 18 months as a consumer app. I met with a cool few teams doing consumer AI (@paulscherer / @ekuyda)

4. MCP came up in literally every conversation. The companies exposing their product as MCP endpoints are getting pulled into deals they never pitched for. The ones that aren't are becoming invisible to agents. This is the new SEO. If agents can't find you, you don't exist. Building products for agents is the new zeitgeist in general.

5. Not uncommon for hot seed rounds to be $25-50 million valuations. I saw a Series A at $450 million

6. If I had a dollar every time someone mentioned "forward-deployed engineer" this trip I could have funded a seed round. It's the hottest role in SF right now. The person who sits between the agent and the customer, making sure everything actually works.

7. The mood around open source shifted. A year ago it felt like open source was chasing the frontier models. Now founders are telling me Gemma and DeepSeek are good enough for 80% of what they need at a fraction of the cost. The "which model do you use" conversation is being replaced by "which model for which task." Model loyalty kinda feels dead.

8. Voice agents came up more than I expected. Multiple founders told me voice is the interface for the next billion users. The billion people who will never type a prompt will absolutely talk to one.

9. The Obsidian community in SF is weirdly intense. Multiple founders showed me their vaults unprompted. Like showing someone your home gym. It's a flex now. The quality of your knowledge base (second brain?) is becoming a status symbol among builders.

10. Maybe it was just the people I met but the age of the founders is shifting. I met more founders over 40 this trip than any trip before and more founders under age 21 than ever before. Founders getting older and younger at the same time.

11. I spoke to a lot of fast-growing startups, VCs and frontier models who are hiring content creators right now.

12. The restaurant scene in SF is actually better than it's been in years. Founders are going out more. Alcohol is out, not surprisingly.

13. SF doesn't feel like the only place anymore. We all have access to the same frontier models. We all read the same X feed. A founder in NYC or Lagos is calling the same APIs as a founder in SoMa. So in the past it felt like SF was always lightyears ahead, doesn't feel that way anymore. It's okay not to live in SF and have BIG DREAMS.

14. The coworking spaces in SF are half empty but the coffee shops are packed. People want to be around people. I had a few startup ideas here....

15. Walking around the Mission I noticed something: the street-level businesses, the taquerias, the barbershops, the laundromats, none of them use any AI at all.

16. I heard the phrase "agent debt" for the first time. Like technical debt but for agents. When you hack together an agent workflow fast and never clean it up, the system prompts conflict, the memory gets polluted, the tools overlap. 6 months later the agent is doing weird things and nobody knows why lol.

17. Met a few people who carry two phones now. One for personal. One that's basically an agent terminal running Telegram or iMessage connections to their agent fleet.

It's always amazing to get that dose of inspiration in SF. I FEEL INSPIRED.

But I'm so happy to be back home, locked in and building.

We're 12-18 months into a shift that will take 15 years to play out. The urgency in every conversation was real.

What an incredible time to be building.

Boris Cherny, the creator of Claude Code at Anthropic, just explained why single-agent workflows are already dead

in this talk he breaks down exactly how the future is teams of agents, not better prompts:

- the 14% you lose to CLAUDE.md before typing a word

- one agent researching. one building. one reviewing. one orchestrating

- the architecture that separates hobbyists from real builders

- the 3 properties every agent team needs to actually survive

if you've been using Claude for more than a month and never left the chat window, you've been using one agent when you could be running a team of them

instead of another show tonight, watch this

make sure to bookmark it before it gets lost in your feed

the guide is in the article below

A 24-year-old ex-OpenAI researcher just turned $225M into over $13.67B in under 2 years.

And his portfolio just revealed something even more extreme than his returns.

Leopold Aschenbrenner was fired from OpenAI in April 2024.

After that, he wrote a 165-page thesis predicting AGI by ~2027.

Then he launched a fund and did something unusual:

He fully positioned around that thesis.

He initially avoided the obvious AI winners:

Zero $NVDA

Zero $MSFT

Zero $GOOGL

Zero $AMZN

Instead, he targeted what AI physically runs on.

His early “AI infrastructure” longs included:

• Bloom Energy $BE

• Lumentum $LITE

• SanDisk $SNDK

• CoreWeave $CRWV

• Iris Energy $IREN

The thesis was simple:

AI isn’t just software.

It’s constrained by:

• power

• bandwidth

• storage

• compute infrastructure

And those bottlenecks were massively mispriced.

The results were explosive:

• Bloom Energy: +1,422%

• Lumentum: +1,331%

• SanDisk: +3,130%

• IREN: +583%

• CoreWeave: +166%

This is what turned his initial $225M into ~ $5.5B by end of Q4 2025.

Fast forward to his latest SEC filing (Q1 2026):

His disclosed exposure has surged to $13.67B equivalent across 42 positions.

A near 3x jump in a single quarter.

But the structure of the portfolio changed dramatically.

He didn’t just stay long AI infrastructure.

He built a two-sided portfolio;

Massive bearish positioning on semiconductors (puts totaling ~$7.46B):

• $SMH ETF PUT: $2.04B

• $NVDA PUT: $1.57B

• $AVGO PUT: $1.01B

• $AMD PUT: $969M

• $MU PUT: $583M

• $TSM PUT: $535M

• $ASML PUT: $494M

• $ORCL PUT: $1.07B

• $INTC PUT: $159M

At the same time, he STILL holds long exposure to the AI infrastructure stack:

• $BE : $878M

• $SNDK: $724M

• $CRWV: $556M

• $IREN: $401M

• $CORZ: $389M

• $APLD: $320M

• $RIOT: $142M

• $CLSK: $104M

• $SEI: $62M

• $TE: $43M

• $KEEL: $38M

• $BTDR: $29M

• $PSIX: $26M

• $WYFI: $20M

• $BW: $19M

• $SHAZ: $18M

• $PUMP: $13M

• $HIVE.NE: $6M

He also added CALL OPTIONS on select names:

• $MU CALL: $422M

• $SNDK CALL: $388M

• $TSM CALL: $354M

• $CRWV CALL: $140M

• $BE CALL: $55M

So the positioning is not a simple “AI is over” trade.

It’s more specific:

He still believes AI infrastructure expands aggressively…

…but thinks semiconductor leaders may have pulled forward too much optimism.

In other words:

He is long the physical buildout of AI

and short the market’s most crowded AI expectations

at the same time.

From $225M → $5.5B → $13.67B…

The real signal isn’t just performance.

It’s that his view of AI has evolved from:

“AI wins”

to

“the winners of AI may not be who the market thinks.”

Are you going to ignore him again?

Anthropic just integrated Harvey AI as a connector inside the same release that ships 12 plugins doing what Harvey does.

Harvey raised $200M in March at $11B. Legora raised $600M Series D last month. Their pitch: legal-specialized AI built on top of frontier models. That value capture only works if the model layer underneath stays neutral.

It didn't.

Tuesday's release: commercial counsel, employment counsel, litigation associate, plus 9 other practice-area plugins. Plus MCP connectors to Westlaw, CoCounsel, Box, Everlaw, DocuSign. The exact workflow stack Harvey and Legora built their valuations on, shipped natively inside Claude.

Then Anthropic integrated Harvey itself. Which makes Harvey a data source feeding into Claude.

The model layer said yes to powering Harvey. The model layer said yes to integrating Harvey. The model layer also said yes to shipping every product Harvey ships.

Per Anthropic AGC Mark Pike, legal is already the #1 power-user job function inside Cowork with 3x the usage of any other function. A single webinar on legal teams using Claude pulled 20,000 registrations.

Legal AI was already running on Anthropic. Tuesday removed the middleman.

The next $11B legal AI valuation is the one nobody raises.

We're still early -- and AI agents lack of persistent memory which makes them poor workers. Some are beginning to build AI workers that can behave like employees. The winners will combine those AI workers into an AI workforce that operates as One. Then shit is going to get real.

Introducing GTM Atlas, a map for modern AI GTM built with some of the best operators in the industry.

A free resource covering the full customer journey, from lead capture to expansion, with the systems thinking that scales with you.

Our first installation features entries from @ElenaVerna, @jamespastan, @kylecnorton, and more.

Plus a curated stack of perks from partners like @NotionHQ, @clay, @WisprFlow, and @meetgranola.

Start exploring: https://t.co/ba9a8aGUmu

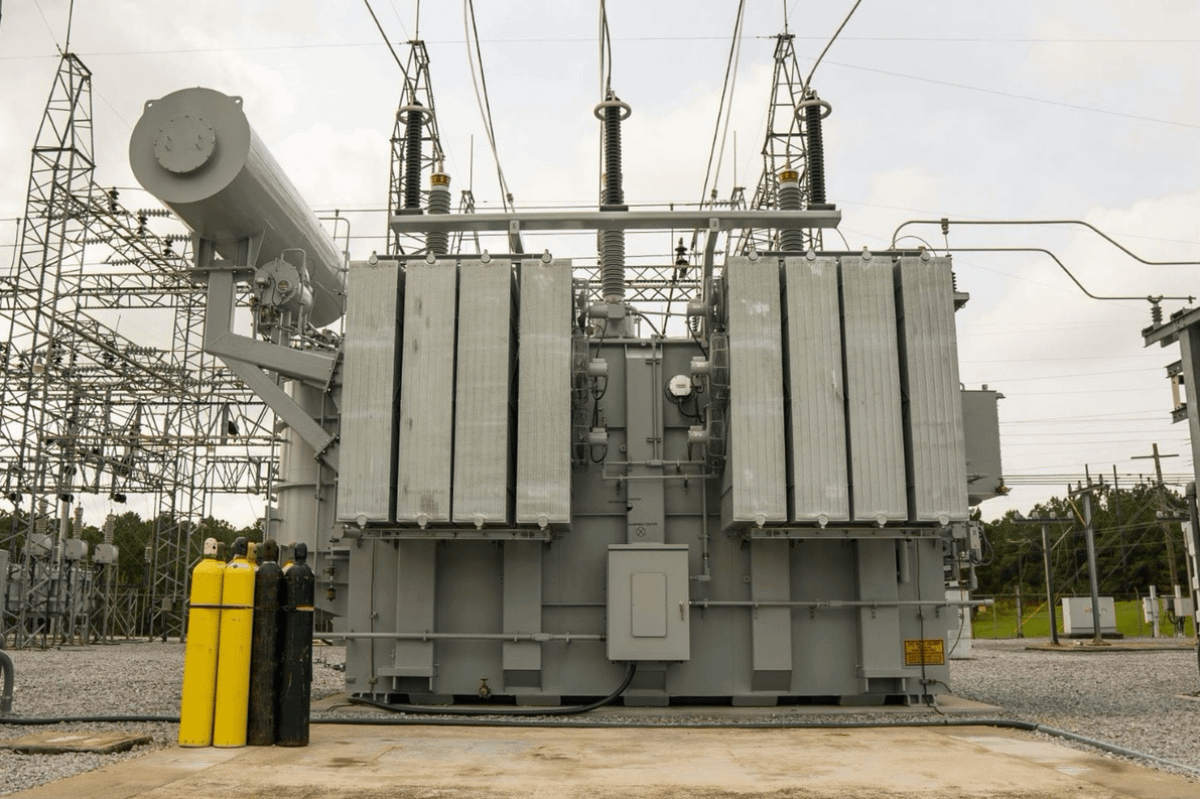

Half of America's AI data centers planned for 2026 are delayed or cancelled. They're waiting on transformers. I build chemical plants. Transformer prices have tripled in the last four years. Lead times are 2 to 4 years. Each new plant we build competes with AI data centers for the same grid equipment. Every large power transformer in America runs on grain-oriented electrical steel. It's made by rolling iron and silicon together until their crystals align in one direction. No other alloy works at utility scale and only one US company makes it: Cleveland-Cliffs. The average large power transformer on the grid is 38 years old. Service life is 40. Amazon, Google, Meta, and Microsoft committed $650 billion to AI infrastructure this year. Nvidia's most expensive GPU is useless without a transformer.