Investors are getting more optimistic about the market. A seven sentiment composite we follow is near its most negative reading possible. The only other time it has been as bearish (too much optimism) in the last five years was in June 2024. While the S&P finished that year higher, there was an 8.5% drop in July-August of that year that helped relieve some of that optimism. This is converging with a very low put volume reading (which is another sign of investor optimism), and a cycle headwind (see charts below). While our longer term sentiment readings aren't yet showing signs of a major top, a pullback should be expected to relieve some of the near term optimism.

Semiconductors are VERY over-extended

$SOX > 60% above the 40-week moving average, way more than most of the prior bubbles.

We've been locking-in gains, the r/r over the next few months isn't favourable. https://t.co/YKr5pL7G2c

Semiconductor stocks are *very* over-extended and due for a pullback.

Quality software stocks are oversold and rallying hard. These are likely to outperform over the following weeks.

S&P average single-stock 1m put-call skew has now collapsed to the lowest level in Goldman Sachs entire dataset.

Translation: Everyone is a bull.

Source: Goldman Sachs

🚨 BILL GURLEY: “I would encourage people to read as much as they can about Anthropic … I don't think they think they're writing software. I think they're midwifing a deity.”

JASON: “I know some of these folks … They believe they're so powerful, that they can create God.”

OpenAI and Anthropic are effectively telling the market they can't solve every problem with a generic AI coworker.

You don't pour billions into massive forward-deployed joint ventures if you think the next model release is going to take care of it.

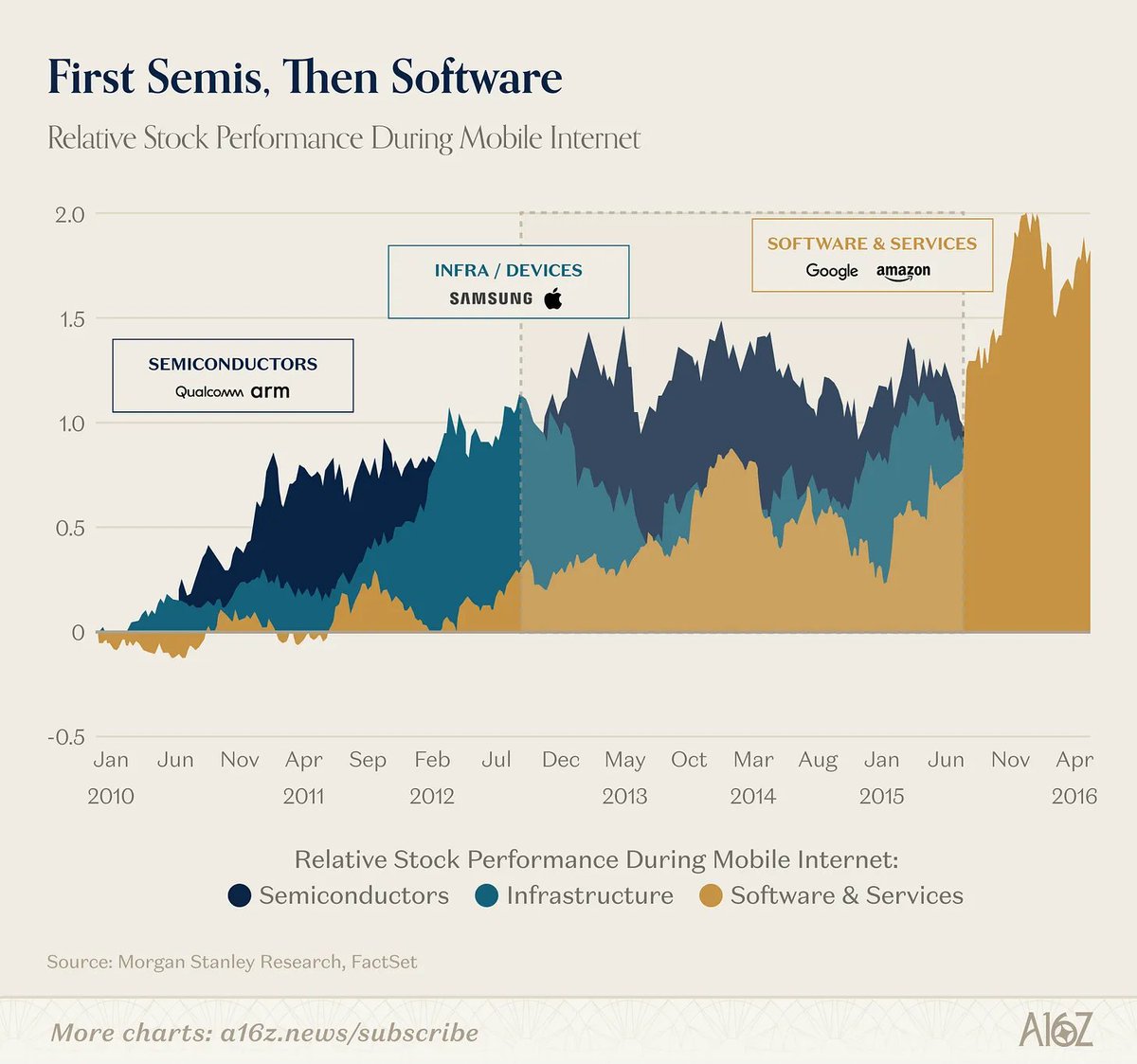

In the cloud supercycle, semis led and software followed (and you didn't need Qualcomm or ARM to tell you the value was migrating up the stack).

In AI, the infra layer itself is telling us the application layer is a separate, massive opportunity they can't fully capture.

a16z's @joeschmidtiv on why the app layer isn't dead: https://t.co/84QN5Mj9T3

🚨 MICHAEL BURRY WARNS THREE UPCOMING IPOs COULD COMPLETELY CRASH THE STOCK MARKET.

Michael Burry reported that the upcoming public listings for SpaceX, OpenAI, and Anthropic are going to pull more capital out of the market than the entire dot-com wave of 2000.

Adjusted for inflation, just these three companies will raise more money than the hundreds of tech firms that flooded the market at the peak of the 2000 bubble.

The historical data from 2000 shows exactly why this is dangerous for stocks.

That year, the market saw 446 IPOs raise a record $108.15 billion. The Nasdaq peaked on March 10, 2000, at the exact moment this massive supply of new shares hit the market, right before crashing 80%.

The crash happened because of a simple liquidity drain.

When giant companies go public, big institutional funds need cash to buy the new shares.

To get that cash, they have to sell their existing stock positions. This creates immediate selling pressure on the most expensive tech stocks.

Today, the setup is identical but much more concentrated. Instead of hundreds of small startups spreading out the drain, just three mega companies are absorbing the market's capital.

This directly impacts current market leaders.

Microsoft has 49% of its $627 billion cloud backlog tied to OpenAI, and Oracle has 54% of its pipeline dependent on it.

The same big funds that need to buy the new IPOs are the ones currently holding these tech giants.

In the first quarter of 2000, the average IPO nearly doubled on its first trading day because cash was easily available.

By the fourth quarter, capital markets dried up.

Gross IPO proceeds collapsed 63% in a single quarter, and average first-day gains dropped to just 14% as companies rushed into layoffs and bankruptcies.

When an unprecedented amount of money is pulled out of existing stocks to fund a single massive IPO wave, the broader market historically runs out of the liquidity needed to sustain its peak.

When we start to see failed breakouts might be the first warning sign. Then when we close below a 5dma. then a 10dma. then a 20dma etc. There will be signs. Right now leaders are working and there are no reasons to be negative outside of the fact price has gone up a bunch.... but that's what things do in a strong bull market. Price goes up.

$NOK — why comps make it a $20 stock TODAY, not someday!

Before we talk about Nokia, Citron owes readers an apology. We've been too negative on the AI data center trade. We missed it and called tops way too early.

Here's what has been learned: the best trade isn't shorting the stocks that already tripled. It's finding the one the market hasn't figured out yet.

That's Nokia. Who cares that it is a 52 week high....looks like it is going higher

While telecom analysts are still valuing Nokia as a slow-growth utility. However, with the Network Infrastructure segment now targeting 18%–20% growth in Optical/IP, the narrative is shifting toward a high performance hardware play.

The whole story in plain English

Nokia makes the equipment that moves data between AI data centers. As AI grows, those highways need to get wider and faster. Nokia builds the highways.

A year ago, Nokia bought a company called Infinera , which meant Nokia went from reselling other people's chips to owning its own chip factories. That's a huge deal. Every other company in this space that owns their own chips (Lumentum, Coherent) trades at a massive premium. Nokia doesn't yet. The market hasn't caught on.

Nokia also hired a new CEO last year Justin Hotard, who came straight from running Intel's AI business. This is not a telecom guy. This is an AI guy now running Nokia. And in October, Nokia signed a $1 billion partnership with NVIDIA that came with an investment.

Last $NVDA investment Citron told you about was $NBIS when it was $20 a share...yes !

Now the numbers. Nokia management has literally told investors what the company will earn in 2028. Add it up and you get roughly 50 cents per share in earnings by 2028. That's their number, not ours.

Here's the thing nobody's doing the math on: every other AI infrastructure stock is already priced based on what they'll earn in 2028. Ciena trades at 49 times those earnings. Coherent at 46 times. Apply the same math to Nokia 50 cents times 49 and the stock is worth $24.50 right now. Today!!

And here's gravy. On last week's earnings call, the CEO said , out of nowhere, nobody asked — "a big milestone later this year with NVIDIA." Seven Wall Street analysts were on that call. None of them followed up. None of them asked what he meant.

When Lumentum got its NVIDIA moment, the stock went from $49 to $960. Nokia just told you its NVIDIA moment is coming this year. And the stock hasn't moved.

That's the whole trade. Nokia is the AI infrastructure stock the market forgot to reprice.

Missed the first wave of this. We're not missing the second.

Short interest on US stocks is at multi-year highs:

Short interest in the median S&P 500 stock is up to 3.0% of market cap, the highest since 2012.

This is DOUBLE the levels seen during the 2020 pandemic.

By comparison, at the peak of the 2008 Financial Crisis, short interest in the median S&P 500 stock stood at 3.8%.

Furthermore, short interest among the most heavily shorted 10% of S&P 500 stocks is up to 8.0% of market cap, the highest since 2018.

Both metrics are now even higher than during the bear market following the 2000 Dot-Com Bubble burst.

Are markets setting up for a short-squeeze?

Call volume at all-time highs is a sentiment data point, not a bullish signal. Put/call ratios at 2-year lows. Hedge funds net short. Retail buying calls into a parabola. The crowd has never been more one-sided. When everyone is positioned for the same move, the risk is always in the direction nobody is hedging.

Tom Lee continues to expect a major market correction later this year.

According to him, the correction will be driven by:

1. Typical midterm seasonality and the uncertainty surrounding it

2. Tight petroleum product inventories that are not being relieved anytime soon, creating energy pressure

3. A large wave of IPOs from SpaceX, OpenAI, and Anthropic, with future lockup expirations creating a supply overhang

Tom Lee also believes the Mag 7 already went through their bear market and will be relatively spared during the broader correction.

He also thinks semiconductor stocks may eventually become a bubble.

There is a near-perfect correlation between US oil prices and US CPI inflation, as shown in our below analysis.

Oil prices have averaged near $100/barrel since March 6th, or 79 days.

The longer this persists, the more inflation we will see.

Asset owners are the only winners.