Morgan Stanley projects SpaceX revenue growing from $18.7B today to $3.4T by 2040.

@PeterDiamandis flagged it immediately as a fundraising tool - Morgan Stanley is likely an IPO underwriter. He's probably right.

But @DaveBlundin's structural point survives: SpaceX's revenue mix has already changed. Starlink ($11B), launch ($4B), and compute rental to Google and @AnthropicAI ($3.2B and growing). That's not a rocket company. That's tech infrastructure.

No one else can match SpaceX's launch economics for deploying AI-1's 1 million satellite Dyson swarm. That compute advantage has no terrestrial equivalent.

SpaceX valuation and the AI compute angle: https://t.co/bXufRxU90D

Source: Moonshots with Peter Diamandis - https://t.co/QALwhWJyth

5 Reasons I am Bullish This Cycle and 5 Caution Signals I am Watching.

Free on my Substack (link below). Please consider subscribing for free market commentary and paid individual stock write ups. First write-up was on $BRUN

https://t.co/s9dsg6cAlN

@BillAckman

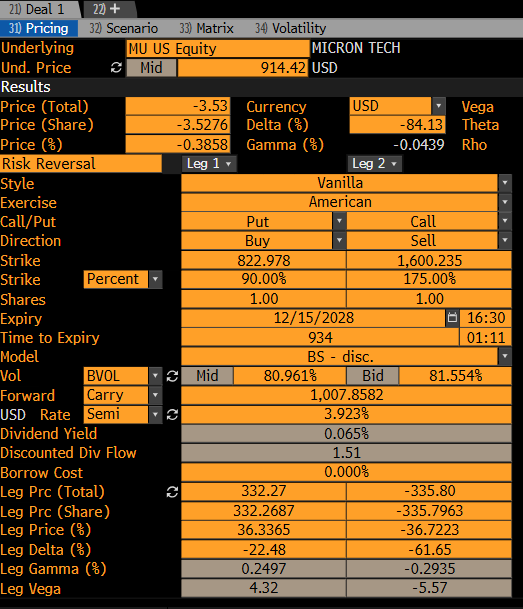

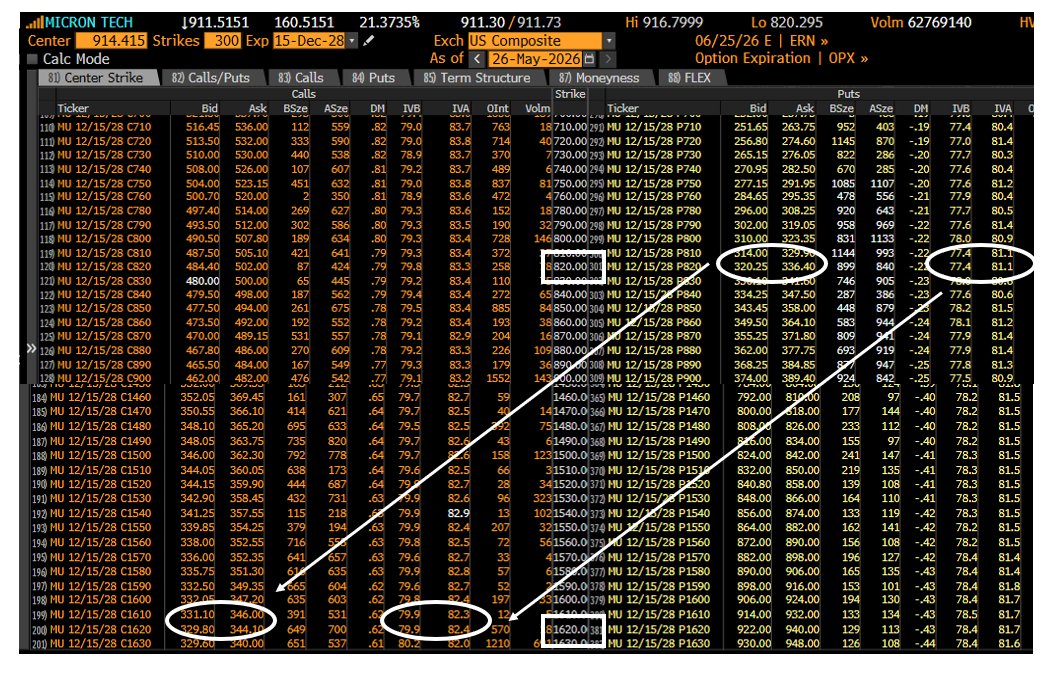

it's collar time... $MU edition, the newest addition to the 1T market cap club.

the collar set up in MU (and other names that has rallied enormously like $SNDK and $INTC) is extraordinary, even if you are paying up for a little for liquidity.

the long-dated vols (Dec'28) are 80. the vol skew is almost completely flat. interest rates are 4%. the stock pays (almost) no dividend. each of these contributes to favorable economics.

you can buy a Dec'28 put option struck 10% below the spot price and finance it by selling a call option 75% above the current price. that's pretty sweet risk/reward that the setup in option prices is providing.

I did an explainer on the economics of collars last year...

https://t.co/nNlbiypm2H

AI datacenters are hitting a physical wall. They cannot scale for inference in today's state; photonics is the only technology that can solve this.

Materials - $SOI $AXTI

Foundries - $GFS $TSEM $TSM

Epitaxy/III-V - $IQE $COHR $LITE $AAOI $SIVE

Testing - $AEHR $TER $FORM

Design - $SNPS $AVGO $MRVL

Packaging - $FN

The write-up below explains why inference cannot scale today, what photonics, SiPho, III-V, quantum wells are, how they work, what each of these companies does, their importance in the supply chain, and how to manage those opportunities.

Do not miss the next big wave of AI hardware 👇

https://t.co/LzsY1Y73n9

CapitalWatch has released its report. It spends a lot of time introducing Tang Hao and Chen Zhi to set the stage for the short thesis.

Tang Hao’s ad spend scenario may indeed be possible, but the claim that Chen Zhi used Array to embed gambling/scam software looks more like speculation.

As for Tang Hao, running ads for gambling apps can be normal—gambling is legal in many countries. CapitalWatch’s point, however, is that Tang Hao is both the advertiser and the publisher, so they argue he is effectively laundering money via a 45% take rate. You can think about what kind of organization would launder money at a 45% take rate—after a few rounds, wouldn’t the money basically be gone?

Of course, one could counter that Tang Hao also owns a 10% stake, so the upside from the share price increase could far exceed the take rate being “skimmed.” But the stock price and ad spend are not directly mapped; there are many variables. Even if you know revenue might increase by low single digits as a result, it’s still very hard to predict whether the stock will go up or down. If it were that predictable, all major clients would end up extremely wealthy.

I find it hard to imagine anyone would accept such a high cost of money laundering.

We’ve previously written a number of detailed reports rebutting the short reportson AppLovin, and they’re well worth reading. $APP

Deep|APP: Further Response to the Short Report

https://t.co/EfPDJtZFvl

Deep|APP: How E-commerce Advertisers View the Short Report

https://t.co/Rq7XM4owoJ

Deep|APP: What is Fingerprinting and Its Impact

https://t.co/3QORTbgbON

Deep|App: Why Can Applovin Retrieve META UUID? Why Can Applovin Do Retargeting?

https://t.co/kBG7Iiij0R

The investment case for $INTC gets thrown around a lot on here but you almost never see any numbers, or valuations.

I figured it was worth spending a bit of time trying to see how the company could look in a couple of years if the cards start falling their way.

Absolutely absurd we got the former head of commodities at Bridgewater and just overall great guy who’s been writing about the silver thesis for over a year to provide this kind of free value of him walking through his thinking of the trade live

Well written man and congrats

@casualtradr@InsideOptions_ Expected this yesterday before their 4th loss & they may not be ready for the 5th.

Pausing martingale in between is worst, as realized losses wipe out earlier gains.

Once started it should be played till the end, either win or wipeout.

Gone!

$RKLB

2026 is most likely going to be a big year for space, for the stock market and therefore for Rocket Lab.

@xbc9stazj is a great follow and has summarised some of the reasons below on why there's still a lot of potential for RKLB. I'm very much on the same page.