Some quick thoughts on Micron $MU earnings tomorrow after the close:

> Estimates are $35B revenue; $20 EPS

I have them reporting $27.90 EPS, ~37% beat. $42.3B revenue, ~21% beat.

I don't think it will be even close and wouldn't be surprised if it is higher.

DRAM pricing is going to keep climbing for the foreseeable future (maybe until 1H27).

If the share price wants to go up post earnings release I believe it will have to show these 3 things:

1. Gross margin. Not a slight gross margin beat, but significant. Estimate is 81% for this quarter, so 83-84% would be even more encouraging.

2. Revenue growth projection. What is the projected QoQ growth for Q4'26? Any signs of QoQ decel in revenue could send the stock tumbling. I expect revenue growth to be robust due to price increases. They are obviously tight on supply and a lot of growth is coming from ASP increase, not surge in bits shipped.

3. What is the news on capacity? More capacity coming online sooner or later? I believe this question is a double edged sword. If Sanjay comes out and says capacity will be added sooner than people think, then it could send a message of margin compression coming soon. If Sanjay comes out and says capacity is tight until 2029/2030, it can either send the share price higher (due to sustainability of high margins) or the market takes it the wrong way as getting too expensive to handle for hyperscalers.

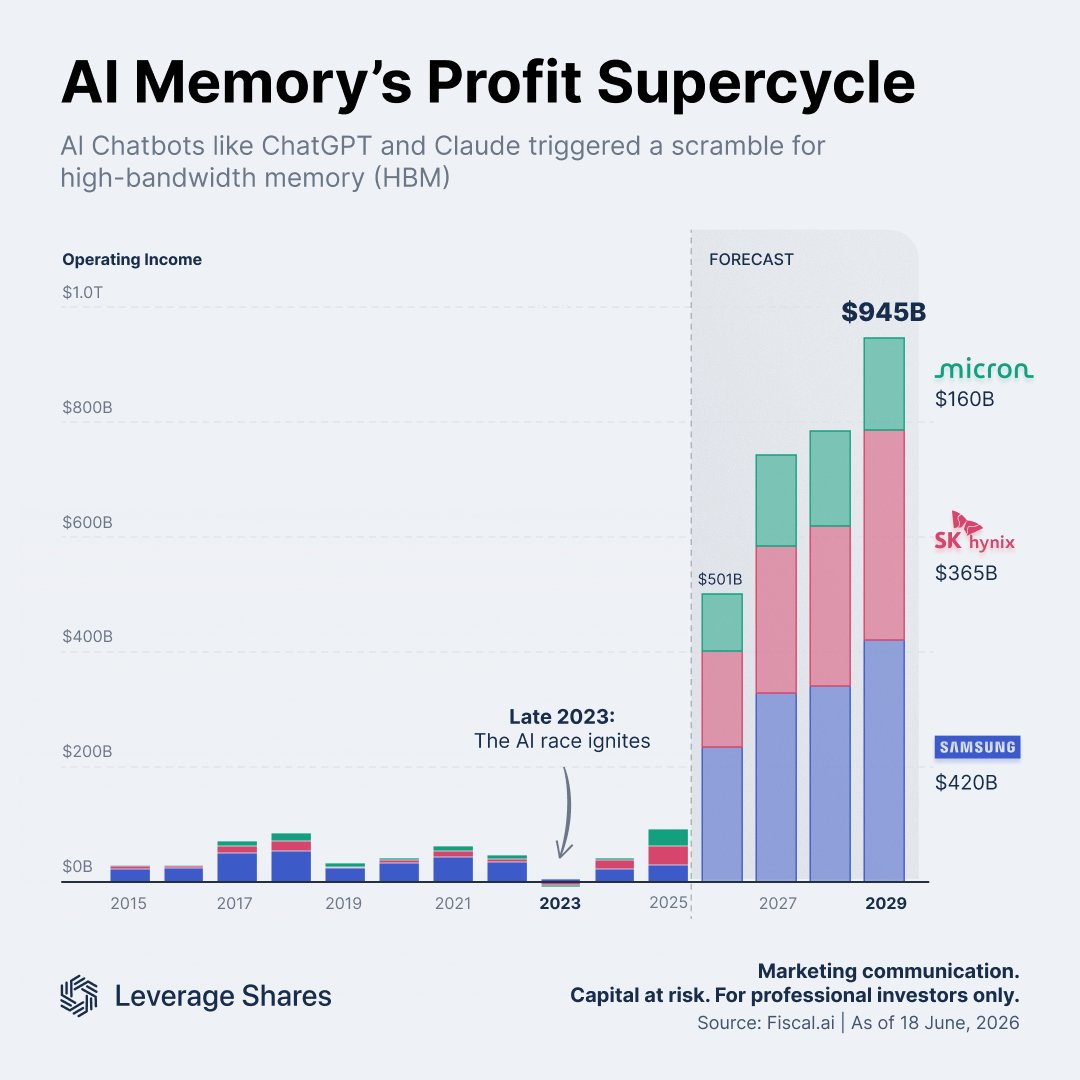

AI's hidden winner? Memory.

As ChatGPT sparked the AI arms race, demand for high-bandwidth memory (HBM) surged alongside it.

Forecasts suggest operating income across Samsung, SK hynix, and $MU could approach $945B by 2029 as AI infrastructure spending accelerates.

The AI memory supercycle is just getting started.

Our full $NBIS model is officially here!

Check out the full report in the first comment.

Since our first model Nebius received a significant $NVDA investment, a very underrated $META backstop as a financing lynchpin, and is nearing the 20 site mark globally.

We continue to build our Nebius model from the ground up using a site by site energization method that we now have visibility to run out through 2030.

Thanks to interviews and events with @daniel_koss@mvcinvesting@romanchernin Tom Blackwell and many other Nebius members and contributors, we gained immense insight into how Nebius continues to execute faster that even our aggressive bull case could image.

While we were directionally correct that mix shift would continue to weigh more towards ai cloud contracts with enterprise and ai natives through the end of the decade, we couldn't imagine that it would be near achieved in 2026.

Our 2030 Base case below illustrates just how forward our expectations for growth have shifted at this rate of execution.

Capacity — Connected MW (base case)

2026: 905

2027: 2,142

2028: 3,964

2029: 4,646

2030: 5,200

Undisclosed data center expansion bucket — Connected MW (base case)

2027: 175

2028: 425

2029: 600

2030: 739

ARR per MW (M, base case)

2026: 9.9

2027: 11.3

2028: 12.8

2029: 13.8

2030: 14.5

Exit ARR (B, base case)

2026: 9.0

2027: 24.2

2028: 50.7

2029: 64.1

2030: 75.4

Recognized revenue (B, base case)

2026: 3.4

2027: 15.8

2028: 36.1

2029: 58.1

2030: 70.3

Gross CapEx (B, base case)

2026: 25.0

2027: 39.4

2028: 59.6

2029: 26.2

2030: 25.2

Cumulative 2026–2030: ~$175B

Funding assumptions (base case)

1. Prepayments, % of CapEx: 55%

2. Core OCF, % of EBITDA: 70%

3. External gap, debt/equity: 85/15

4. Blended interest cost: 5.5%

Funding outcomes (B, cumulative 2026–2030, base case)

1. Prepayments: ~95

2. Core OCF ex-prepayments: ~49

3. Debt raised: ~34

4. Equity raised: ~6

5. Ending debt: ~43

6. Ending cash: ~20

Adjusted EBITDA margin (base case)

2026: 40%

2027: 42%

2028: 44%

2029: 45%

2030: 45%

Implied 2030 adj. EBITDA: ~$32B

D&A (B, base case)

2026: 2.9

2027: 8.1

2028: 16.2

2029: 23.1

2030: 27.3

Share count (base case)

Ending diluted shares: ~339M

Base case scenario probability weight: 55%

Thank you to our premium members for your massive support in bringing this refresh so quickly.

Price targets, our portfolio allocation, present value calculations, and our buy/hold/trim/sell zones are now live.

Your margin is my opportunity: AI version…

The biggest surprise of 2026 is that the capability gap between the best open-weight/source models and the best closed models has narrowed much faster than the pricing gap. The pricing gap remains enormous while the capability gap is quite narrow.

What does this means in practice?

For a company consuming 1 billion input tokens and 1 billion output tokens per month:

GPT-5.5 Pro: ~$105,000

Claude Opus 4.8: ~$30,000

DeepSeek V4 Pro: ~$5,220

DeepSeek R1: ~$2,740

I asked ChatGPT what it thought about this and it answered as follows:

“If I were building a company today, the economic frontier would look roughly like:

DeepSeek V4 Pro / R1 for high-volume inference.

Claude Opus for premium agent workflows where reliability matters.

GPT-5.5 Pro only for workloads where its incremental capability demonstrably produces enough business value to justify a 20–40× token premium.”

Most CEOs have no idea that, instead of this nuanced approach, their teams are running amok internally by picking the most expensive models in most cases and burning through massive budgets with zero governance, audit ability and control.

As control planes like our Software Factory become more standard, you can expect the run rate revenue growth of the frontier labs to go down meaningfully and the revenues of the open models to skyrocket.

Why? Because we can implement the nuanced approach above and be agnostic to model - instead focusing on customer intent, model task and cost management among other things.

OpenAI and Anthropic are effectively telling the market they can't solve every problem with a generic AI coworker.

You don't pour billions into massive forward-deployed joint ventures if you think the next model release is going to take care of it.

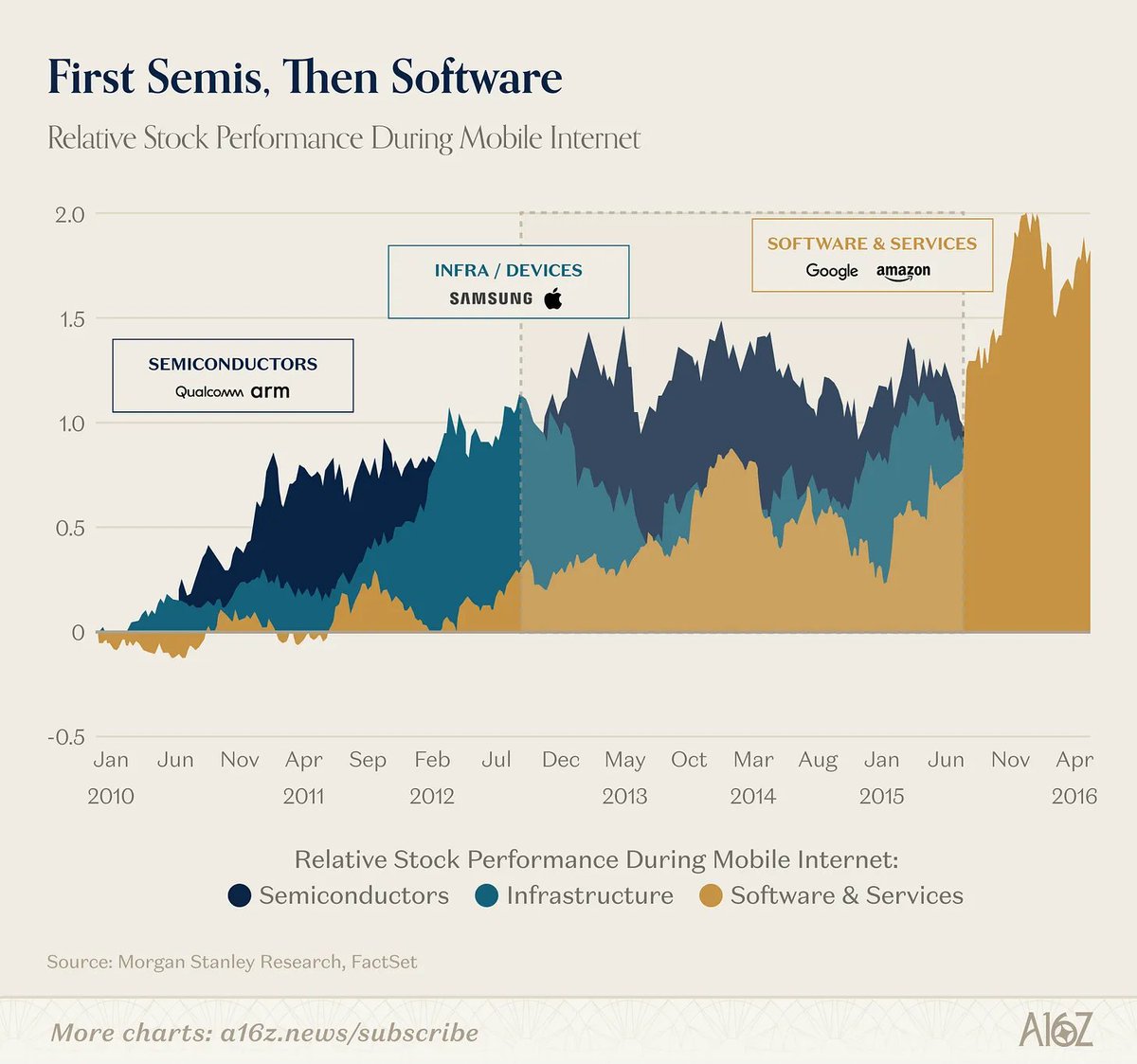

In the cloud supercycle, semis led and software followed (and you didn't need Qualcomm or ARM to tell you the value was migrating up the stack).

In AI, the infra layer itself is telling us the application layer is a separate, massive opportunity they can't fully capture.

a16z's @joeschmidtiv on why the app layer isn't dead: https://t.co/84QN5Mj9T3

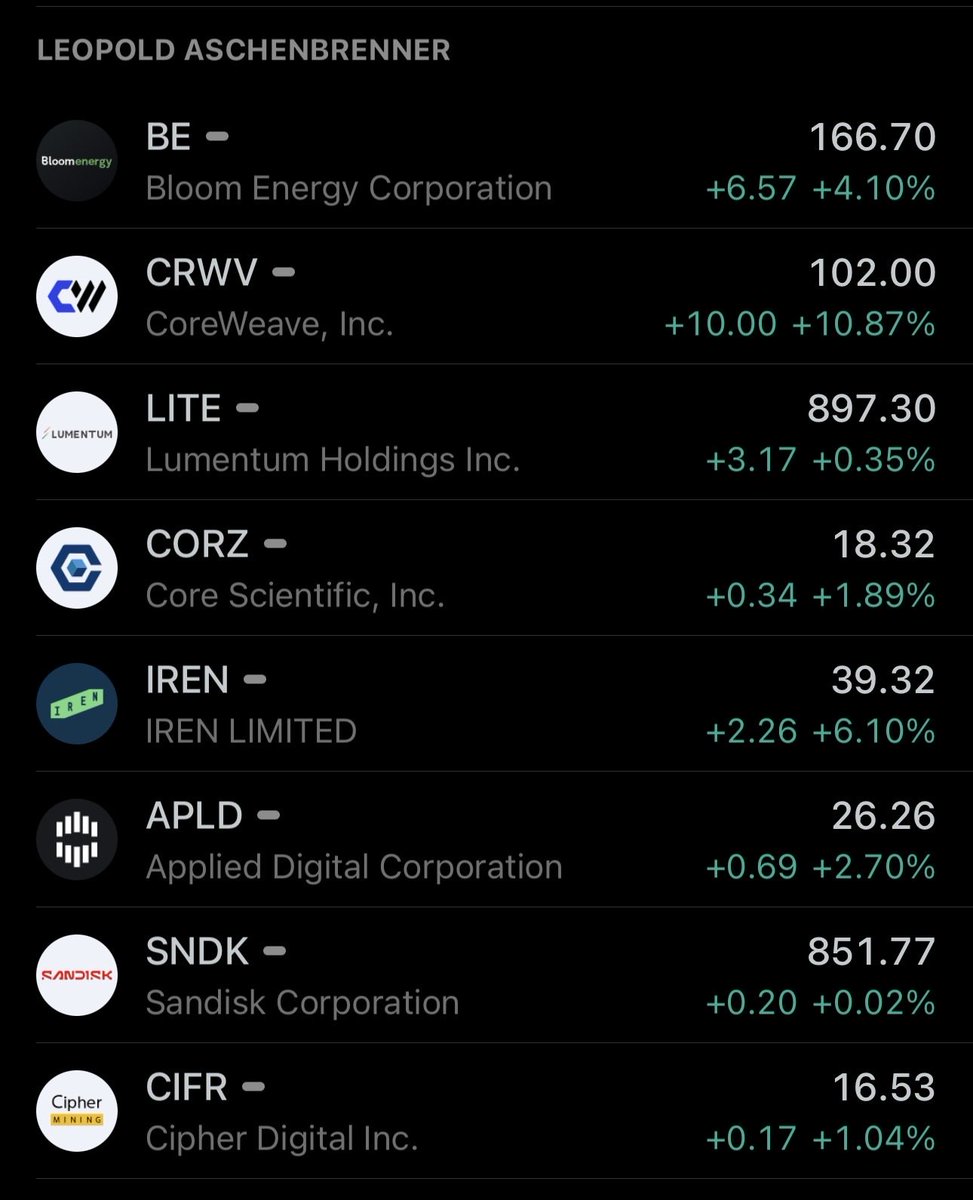

JUST IN: Leopold Aschenbrenner just updated his stock portfolio for his Situational Awareness Fund

This is every SINGLE STOCK he owned so far the end of Q1 (This does not include options)

$878.7M of Bloom Energy $BE

$724.4M of Sandisk $SNDK

$556.1M of CoreWeave $CRWV

$401M of Iren Limited $IREN

$389.1M of Core Scientific $CORZ

$320M of Applied Digital $APLD

$142.2M of Riot Platforms $RIOT

$104.5M of Cleanspark $CLSK

$62.5M of Solaris sei-network:native

$43.9M of T1 Energy $TE

$38.8M of Bitfarms

$29.8M of Bitdeer $BTDR

$26.3M of Power Solutions $PSIX

$21M of Corning $GLW

$20.9M of WhiteFiber $WYFI

$20.2M of $AMD

$19.9M of Babcock and Wilcox $BW

$18.1M of SharonAI $SHAZ

$13.1M of Propetro $PUMP

$10.3M of $SMH

$8.9M of Intel $INTC

$7.6M of Taiwan Semi $TSM

$6.4M of Hive Digital $HIVE

$6.1M of $ASML

$5.9M of Micron $MU

The four most dangerous words in investing are, “This time is different.”

The twelve most dangerous words in investing are, ‘The four most dangerous words in investing are, “This time is different.”’

Here's a bunch of random 30 US-available random stocks I like today and why:

1. $INTC - America's hope for foundry, national security

2. $MRVL - scales rev from future maia asics and add ons like cpo, they do everything lost count

3. $TSM - backbone of semis/ai

4. $COHR - They do everything vertically integrated + captures optical cycle

5. $RKLB - the final frontier of space will be around 5 years from now and 20 years from now.

6. $DRAM - memory exposure for samsung/sk hynix

7. $AVGO - hyperscalers dont like nvidia gpu tax

8. $AMZN - nobody can compete against the overnight shipping of toilet paper. robotics will lower opex over time

9. $ARM - AGI CPUs scale revenue quite a bit over the next decade

10. $TSEM - you're going to need a foundry for light based stuff

11. $IBIT - bitcoin, we all know by now

12. $NBIS - i think it's the next AWS. Also they do self-driving cars with uber, own scaling DB companies, data labeling. It's almost like a mini Google.

13. $GOOGL - youtube is not going away, gemini is great. they're vertically integrated with TPUs and fund buildout with operating income so i like it.

14. $AMKR - super facilities coming online in late 2027-2028. benefits from made in america

15. $HOOD - i dont like short term, but long term i'm a fan of Robinhood since they captured retail + have more products like banking, etc that they're scaling up. product innovation is wild.

16. $CRCL - I happen to really like stablecoins and see them as the future for both payments/holding (depends on clarity act)

17. $META - people aren't going to stop using instagram or whatsapp, or others anytime soon.

18. $LITE - $GOOGL TPU exposure decently high part of BOM. As long as Google's AI program keeps running I think $LITE will do well.

19. $LPTH - Germanium and China export controls will always be an issue so US made engineered alternatives will always be important

20. $FN - Someone needs to assemble optical stuff

21. $JBL - same as above, but added with ip from Intel's SiPh acqusition so might end up like innolight?

22. $MP - American rare earths program is extremely important, similar to $INTC national security risks

23. $HIMS - Okay here me out they just acquired a ton of companies, and at $19 they have global DTC channel. short sellers really hate this company, but I think it's actually promising as a contrarian long

24. $SMTC - LRO/LPO transition

25. $POWL - US alternative to hammond for switchgear DC type bottleneck

26. $VPG - Humanoids will be a thing down the road maybe 2027-2028, this makes the sensors.

27. $MOG.A - Feels like i see them everywhere in robotics, to spacex supply chains

28. $MSFT - At $375, one day we'll look back and see this as a buying opportunity.

29. $CVX - oil might crash after war but these oil companies are going to be extremely important, especially when Venezulea is a goldmine.

30. $XLU - i think rate cuts might be back online, we need power/grid for AI so these names will always be improtant from $CEG to $NEE

Just throwing out other thoughts aside from $AAOI and $AEHR.

LLM Knowledge Bases

Something I'm finding very useful recently: using LLMs to build personal knowledge bases for various topics of research interest. In this way, a large fraction of my recent token throughput is going less into manipulating code, and more into manipulating knowledge (stored as markdown and images). The latest LLMs are quite good at it. So:

Data ingest:

I index source documents (articles, papers, repos, datasets, images, etc.) into a raw/ directory, then I use an LLM to incrementally "compile" a wiki, which is just a collection of .md files in a directory structure. The wiki includes summaries of all the data in raw/, backlinks, and then it categorizes data into concepts, writes articles for them, and links them all. To convert web articles into .md files I like to use the Obsidian Web Clipper extension, and then I also use a hotkey to download all the related images to local so that my LLM can easily reference them.

IDE:

I use Obsidian as the IDE "frontend" where I can view the raw data, the the compiled wiki, and the derived visualizations. Important to note that the LLM writes and maintains all of the data of the wiki, I rarely touch it directly. I've played with a few Obsidian plugins to render and view data in other ways (e.g. Marp for slides).

Q&A:

Where things get interesting is that once your wiki is big enough (e.g. mine on some recent research is ~100 articles and ~400K words), you can ask your LLM agent all kinds of complex questions against the wiki, and it will go off, research the answers, etc. I thought I had to reach for fancy RAG, but the LLM has been pretty good about auto-maintaining index files and brief summaries of all the documents and it reads all the important related data fairly easily at this ~small scale.

Output:

Instead of getting answers in text/terminal, I like to have it render markdown files for me, or slide shows (Marp format), or matplotlib images, all of which I then view again in Obsidian. You can imagine many other visual output formats depending on the query. Often, I end up "filing" the outputs back into the wiki to enhance it for further queries. So my own explorations and queries always "add up" in the knowledge base.

Linting:

I've run some LLM "health checks" over the wiki to e.g. find inconsistent data, impute missing data (with web searchers), find interesting connections for new article candidates, etc., to incrementally clean up the wiki and enhance its overall data integrity. The LLMs are quite good at suggesting further questions to ask and look into.

Extra tools:

I find myself developing additional tools to process the data, e.g. I vibe coded a small and naive search engine over the wiki, which I both use directly (in a web ui), but more often I want to hand it off to an LLM via CLI as a tool for larger queries.

Further explorations:

As the repo grows, the natural desire is to also think about synthetic data generation + finetuning to have your LLM "know" the data in its weights instead of just context windows.

TLDR: raw data from a given number of sources is collected, then compiled by an LLM into a .md wiki, then operated on by various CLIs by the LLM to do Q&A and to incrementally enhance the wiki, and all of it viewable in Obsidian. You rarely ever write or edit the wiki manually, it's the domain of the LLM. I think there is room here for an incredible new product instead of a hacky collection of scripts.

Lazarus Group is the collective name for all DPRK state sponsored cyber actors.

The main issue is everyone groups them all together when the complexity of threats are different.

Threats via job postings, LinkedIn, email, Zoom, or interviews are basic and in no way sophisticated (DPRK groups: DPRK IT workers, Contagious Interview, Dangerous PW/Bluenoroff/SapphireSleet).

The only thing about it is they’re relentless.

If you or your team still falls for them in 2026 you’re very likely negligent.

The ONLY two DPRK groups you will see regularly doing sophisticated crypto attacks are TraderTraitor (Bybit/DMM) & AppleJeus (Radiant/Drift)

I always see companies write about how they stopped the most elaborate attempt by Lazarus Group and it ends up being a basic attempt by a low iq subgroup….

Introducing TurboQuant: Our new compression algorithm that reduces LLM key-value cache memory by at least 6x and delivers up to 8x speedup, all with zero accuracy loss, redefining AI efficiency. Read the blog to learn how it achieves these results: https://t.co/CDSQ8HpZoc

NATO is testing live cockroaches as AI-powered spy drones.

Incredible AI engineering, but also something I kinda wish I hadn't learned about:

> Swarm Bio-tactics wired real cockroaches with electronic backpacks containing AI hardware, radios, cameras, and microphones.

> Cockroaches are steered by sending electrical signals directly into the insect's nervous system

> They can crawl through rubble, tunnels, and spaces where drones can't fly, and troops shouldn't go, transmitting data back the entire time.

> Within one year, they went from concept to field-validated systems with paying NATO customers, including the German military.

The qualities that make them useful for military recon (small, silent, nearly undetectable) are exactly what make them creepy.

...International laws weren't written with cyborg insects in mind.

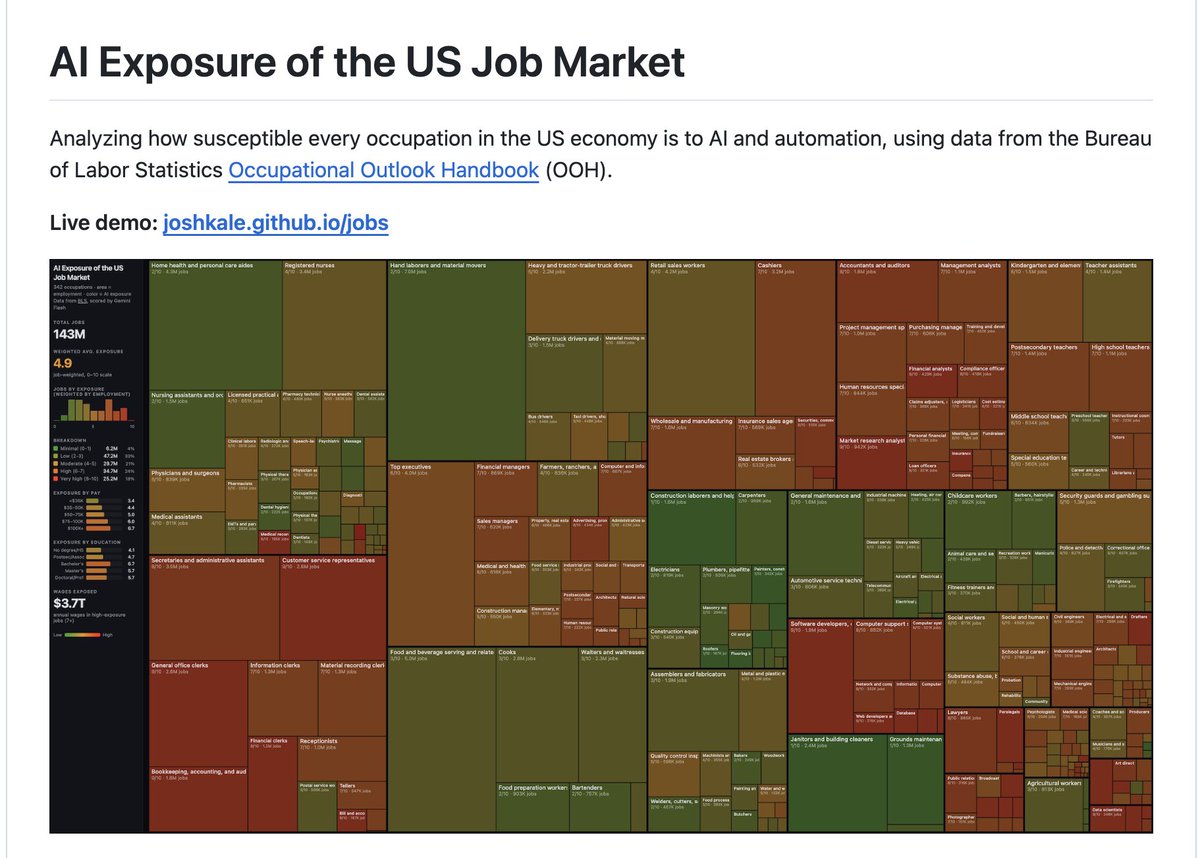

Karpathy scored every job in America on AI replacement risk. Then he deleted it.

It went viral Last night. Elon replied. News outlets picked it up. So I brought it back to life.

Cloned the entire repo to play with before it went down. Every file. The scoring data, the full pipeline, the interactive visualization. All of it.

It's back up here: https://t.co/lpD3LVTNnr

The data was too noteworthy to let vanish. 342 occupations scored 0-10 on how much AI will reshape them. Average exposure across the entire US economy: 5.3/10.

If your job lives on a screen, it's worth taking a look.

Introducing Cline Kanban: A standalone app for CLI-agnostic multi-agent orchestration. Claude and Codex compatible.

npm i -g cline

Tasks run in worktrees, click to review diffs, & link cards together to create dependency chains that complete large amounts of work autonomously.

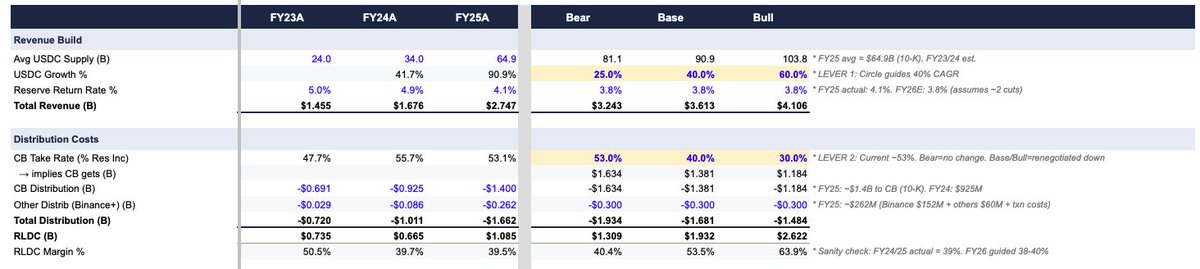

Loaded up the truck on CRCL today. Wrote the pitch at $70, saw it go to $50, didn't enter & watched it rip to $130 without me and now a knee jerk reaction from the market to dump it to $100 for a god given entry

CRCL is one of those stocks with a pretty strong adverse reaction. Lots of bears with very valid points:

- Tether IPO

- Losing $ to CB distribution

- CRCL team don't execute like HOOD / has negative optics similar to CB

But IMO that just means more room to grow if those levers get changed - it's adversely priced for failure right now, which makes the wall of worry that much steeper to climb. The bull case is real

- This bill has ST pain for USDC (Assumed TVL loss due to farmers) but has LT stronger outcome

- Second order effect = Can re-negotiate CB distribution ++ gives leverage to CRCL for the negotiations

- Stablecoins as still the best thesis (Even Druckenmiller is bullish stablecoins) ; CRCL remains the only pure play

IMO CRCL boils down to 2 levers at this point in time - USDC Growth Rate and % Cut to Coinbase; modelling that out (Claude is pretty insane) you get to build a pretty good bear / base / bull scenario.

At the most bearish scenario you basically had CRCL trading at mid ~50s (30x multiple) which basically means the market was pricing in the worst case scenario for CRCL

Anyways, all in all I think it's worth a punt